So much for a rerun of the 2016 post-election U.S. stock market rally.

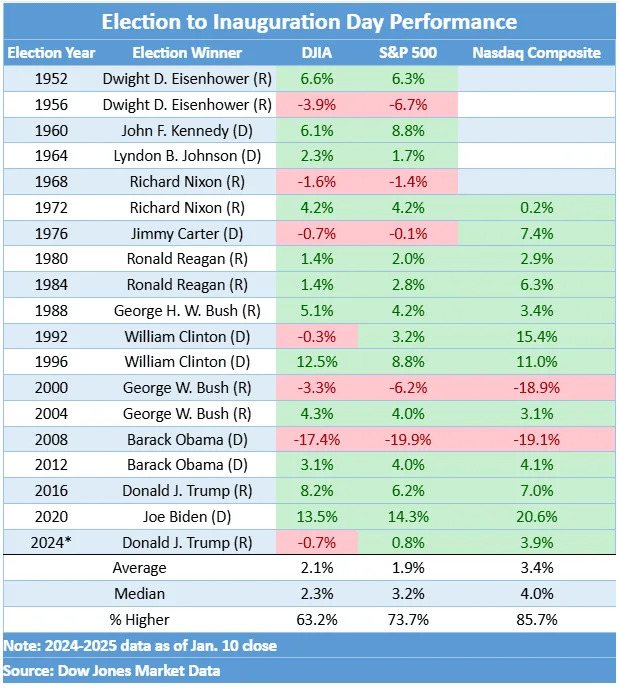

The S&P 500 index SPX is clinging to a gain of just 0.8% since Election Day on Nov. 5, threatening to erase the “Trump bump” investors attributed to Donald Trump’s victory. The performance is on track to be the weakest Election Day-to-Inauguration Day run since the run-up to Barack Obama’s inauguration in 2009 amid a global financial crisis.

It’s also in contrast to 2016, when Trump’s election victory caught investors by surprise. The S&P 500 went on to rally 6.2% over the stretch between election day and inauguration as investors cheered the prospect of corporate tax cuts and deregulation.

As the table above shows, the Dow Jones Industrial Average DJIA has already turned its post-election gain into a loss. So what gives? It looks like the element of surprise might be rather important.

Trump hadn’t been expected to beat Democrat Hillary Clinton in 2016. When he did, stock-index futures initially wobbled, but then rallied. The surge gathered momentum as investors piled into bets on sectors and industries expected to benefit from Trump’s expected policies, stoking animal spirits.

This time around, the race between Trump and Vice President Kamala Harris was seen as too close to call, but betting markets were pointing to a likely Trump win in the weeks ahead of the election, and investors had already followed their cue.

The potential extension — if not deepening — of those tax cuts, along with another round of deregulation, was expected by many to fuel a Trump bump redux. And initially it did. The S&P 500 gapped higher on Nov. 6, the day after the election, and renewed a pre-election run, topping out at a record close of 6,090.27 on Dec. 6, up 5.3% from its Election Day close.

But there was another trade taking place at the same time. Investors were selling bonds, triggering a spike in Treasury yields, which move opposite to price. Surging yields and surging stocks don’t usually go together, seeming to underline a sense of euphoria around stocks.

They’re not rising together anymore. The backup in yields has continued, increasingly hurting some of the most rate-sensitive bits of the stock market. That includes companies with small capitalizations, seen as a prime beneficiary of the Trump victory, which have tumbled below their election day close and are now in correction territory, having dropped more than 10% from their Nov. 25 peak.

The rise in Treasury yields also began in the run-up to the election, after the rate on the 10-year note BX:TMUBMUSD10Y had fallen to just below 3.59%. Investors debated the cause, with some attributing it to the fear that while neither Harris nor Trump would be inclined to rein in a growing fiscal deficit, Trump’s pro-growth policies would be increasingly likely to attract the ire of so-called bond-market vigilantes.

Key Words: Paul Krugman thinks bond yields may be rising due to an ‘insanity premium’

Skeptics question whether budget fears have been the primary driver of the backup in yields.

“I think the most recent episode we’ve had in yields is more about inflation data than concerns about the fiscal outlook…when it comes to the fiscal outlook, I’m not sure how much has changed,” said John Belton, portfolio manager at Gabelli Funds, in a phone interview.

The so-called DOGE, or department of government efficiency, initiative led by Elon Musk and Vivek Ramaswamy, was seen at least blunting concerns about deficits, he said. On the other hand, uncertainty around the effects of tariff and immigration reforms may have served to stoke inflation worries somewhat.

Opinion: Why Elon Musk had to drop his ‘DOGE’ pledge to cut $2 trillion from the federal budget

And then there’s the Federal Reserve, which delivered a 50 basis point interest rate cut to kick off a monetary easing cycle in October, citing concerns over the jobs outlook, following it up with two 25-basis point cuts in November and December.

Steve Ricchiuto, chief U.S. economist at Mizuho Securities, said the bond market’s “adverse reaction to the 100 basis points worth of rate cuts executed since September suggest policy makers have lost some credibility by focusing more on the labor market side of its dual mandate rather than on its inflation objective.” The associated sell-off in the coupon portion of the yield curve also argues against additional rate cuts in 2025, as does the fact that inflation appears to have bottomed out well above the Committee’s 2% target.”

And indeed, Friday saw yields surge because a much hotter-than-expected December jobs report put prospects for further rate cuts by the Federal Reserve in doubt. The 10-year yield finished up 9.2 basis points at 4.772%, its highest since Nov. 1, 2023. Stocks stumbled as a result.

See: U.S. stocks got clobbered Friday despite a blockbuster jobs report. What’s going on?

Stock-market investors are demonstrably worried about those rising yields, with the 10-year rate seen on its way toward 5% and possibly beyond. Expectations for further Fed rate cuts have been sharply curtailed, and some economists and analysts expect the next move to be a hike.

It isn’t all gloom. Belton argued that “were in a pretty good place here for stocks.”

Economic fundamentals — look at that hot jobs report after all — remain good, he said. And deregulation and other elements of the Trump policy agenda “are reasons to be excited,” along with other developments, including the growing adoption of artificial intelligence.

High stock valuations are a constraint, he said, but the “base case” is for market gains in line with corporate earnings growth and the willingness of investors to simply pay more for each dollar of earnings that could still provide a double-digit percentage lift.

Meanwhile, analysts at Bespoke Investment Group urged against getting too caught up in the reaction to a stronger-than-expected jobs report because it “is not going to be something investors will be thinking about” in a few months.

“In 10 days, when the new administration takes over the White House, investors will have dozens of new issues to focus on ,” they wrote Friday afternoon. “This is to say, if you’re contemplating major changes to your portfolio today because of Biden’s final jobs number, it may be better to take the rest of the day off and start your weekend early!”

Read: Dow sees worst start to a year since 2016 as Fed rate-cut hopes fade for 2025