FTR’s 2025 Transportation Outlook forecasts gradual growth

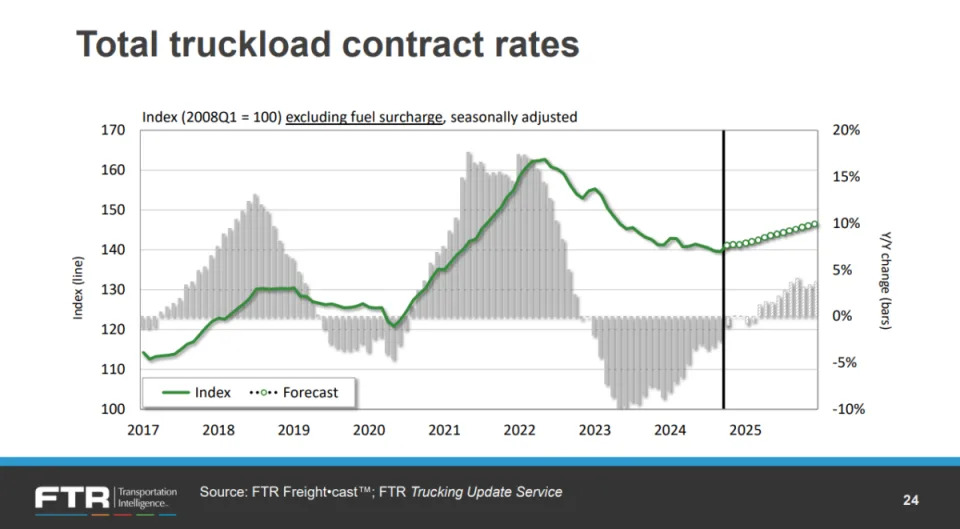

In a recent webinar , Avery Vise, vice president of trucking at FTR Transportation Intelligence, outlined the company’s optimistic outlook for the freight market in 2025. Vise emphasized that while contract rates have softened over the past quarter, expectations for 2025 remain positive.

Vise noted that contract rates have “bottomed out” and are projected to begin rising in the coming months. By the end of the year, FTR forecasts a 5% year-over-year increase, translating to a total contract rate increase of approximately 2%. This gradual improvement is seen as a welcome development for carriers, though Vise cautioned that it won’t mirror the significant spikes observed in 2020 or 2021.

Spot rates are also expected to experience a steady climb, with a projected increase of 5.5% to 6% in 2025 – “Nothing to get overly excited about, but certainly welcome from a carrier perspective,” Vise wrote, indicating a balanced and sustainable rate environment.

Key takeaways for trucking fleets include the anticipation of tighter capacity, despite current labor numbers showing there was an increase in drivers post-pandemic. Vise explained, “Based on the official data we have as of today, we clearly have more drivers than we had before the pandemic.”

Those numbers may be subject to change when revisions come out in the coming months. Heavy Duty Trucking’s Deborah Lockridge wrote, “But hold on – as Vise explained in his column for HDT last month , the current labor numbers are based on monthly estimates. More accurate numbers come from the Quarterly Census of Employment and Wages (QCEW), which takes longer to compile, so capacity likely is somewhat tighter than the numbers suggest.”

Additionally, Vise highlighted that active truck utilization has improved and is expected to continue rising, reaching around 94%-95% by the end of 2025. However, he noted that this level is still below the utilization rates seen in previous years like 2021 and 2018.

Advanced Clean Fleets rule gets a CARB crash following waiver withdrawal

The California Air Resources Board (CARB) recently announced it has withdrawn its request for a federal waiver to implement the state’s Advanced Clean Fleets Rule . The sought-after waiver from the Environmental Protection Agency was submitted back in November 2023 and would have allowed CARB to require fleet operations in the state to achieve 100% zero-emissions fleets between 2035 and 2040 depending on fleet size, truck weight and other factors .

For carriers operating in the state, drayage fleets were under the most aggressive timeline had the rulemaking been implemented. FreightWaves’ John Kingston writes , “The most pressing requirement under the ACF was to be the rule that only zero-emission vehicles could be added to the state’s drayage registry starting Jan. 1, 2024. CARB said it would not enforce that requirement while the fate of the ACF waiver was undetermined but that it reserved the right to enforce it retroactively once a waiver was granted. With a waiver no longer coming, it is unclear what happens to that requirement.”

Beginning with the 1970 Clean Air Act, the EPA has granted waivers to California for decades, allowing it to enact tougher pollution limits than the federal government. An added caveat is that once California enacts a tougher standard, federal law allows other states under certain criteria to adopt California standards as their own. The recent news around Daimler’s halting and resuming the sale of Class 8 trucks in Oregon put a spotlight on that not-always-smooth process.

In the case of California, two factors impacted its decision to withdraw its request. The first is that the incoming Trump administration is expected to revoke such waivers. The second is that the state simply ran out of time.

This is not expected to impact the existing EPA Phase 3 rulemaking, which requires stronger standards to reduce truck greenhouse gas emissions beginning in 2027 .

Market update: Cass December data shows freight volumes drop, rates firm up

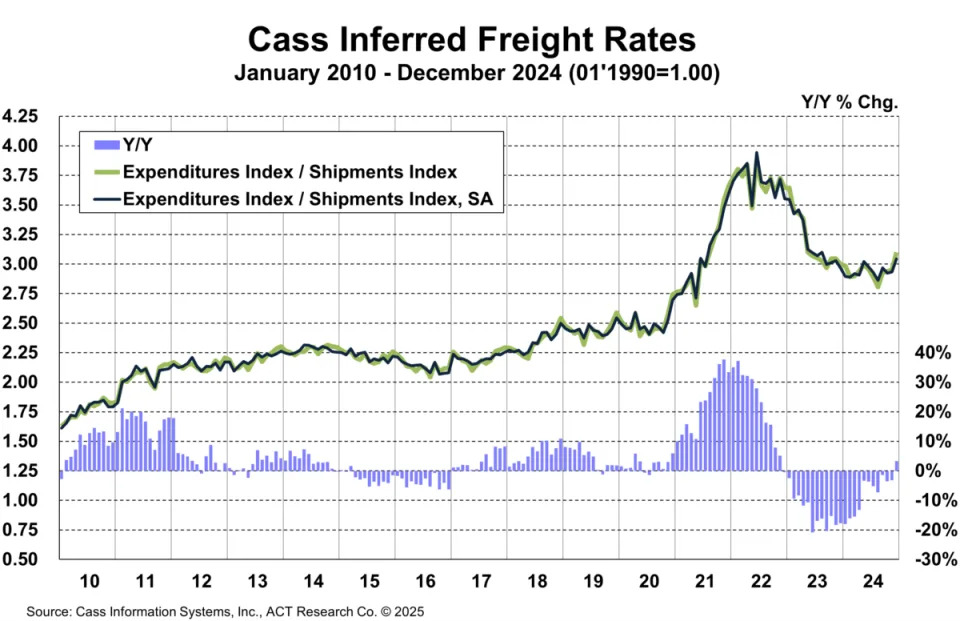

On Tuesday, freight audit and payment provider Cass Information Systems released its December Cass Transportation Index which saw freight volumes in the for-hire space reach their lowest December levels since the early days of the pandemic. However, prices are rising. The Cass Inferred Rates index, which measures domestic freight costs across all modes, is up year over year, for the first time in the past two years.

The shipments component fell 7.3% m/m in December, with half of the decline being attributed to seasonality. Seasonally adjusted, the index was down 3.1% m/m, erasing the 2.8% m/m gain from November. Compared to the previous year, shipments fell 6.5% in December, the largest decline since January 2024. Tim Denoyer, vice president and senior analyst at ACT Research, wrote in the report, “Ongoing capacity additions are keeping pressure on the for-hire market, and the normal seasonal pattern would have the index down about 6% y/y in January.”

Freight expenditures also took a dip. The index that measures total freight spend fell 2.6% m/m in December, down 3.4% y/y. Denoyer added, “The decline was from shipments, which fell 7.3% m/m, and we infer rates rose 5.1% m/m in December in the fourth straight price increase.”

The inferred rates component, which rose 5.1% m/m in December, posted a gain of 3.7% seasonally adjusted and 3.3% year over year. Denoyer continued, “Based on the normal seasonal pattern, this index will remain positive y/y in January and is headed for gains in 2025.”

Looking ahead, the report notes that winter weather is driving significant spot activity in January. Denoyer concludes that “the supply response in the past couple of months has been interesting. While lower Class 8 supply over the past several months supports a return to rate increases in 2025, the capacity additions to come will be considerable.”

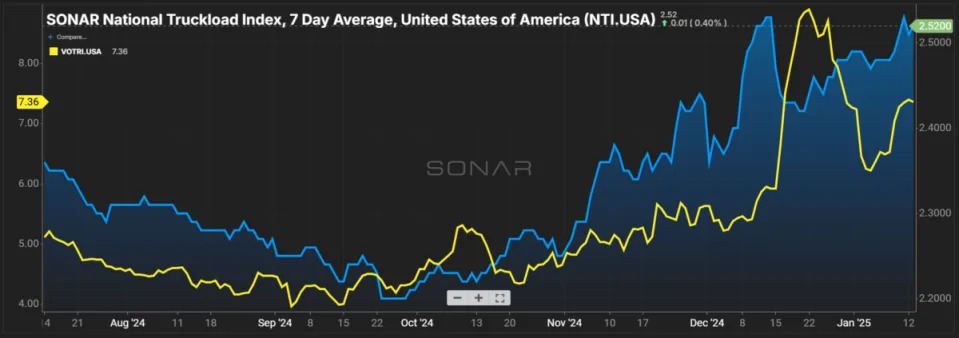

SONAR spotlight: Dry van spot rates’ slow but steady climb

Summary: Dry van spot market and tender rejection rates resumed a sustained uptick following a brief pause for New Year’s. Dry van outbound tender rejection rates rose 83 basis points week over week from 6.53% on Jan. 6 to 7.36%. Looking at seasonal movements, VOTRI now more closely resembles rates from 2019 and 2020, when tender rejection rates were at 8.08% and 7.21%, respectively. It’s a notable improvement from the past two years when VOTRI ranged from 3.98% in 2023 to 4.36% in 2024.

Spot market rates also saw an uptick, with the SONAR National Truckload Index, 7-Day Average increasing 4 cents per mile all in w/w from $2.48 on Jan. 6 to $2.52. Dry van spot rates have nearly regained their month-over-month high of $2.53 per mile on Dec. 14. A positive sign for dry van rates is the sustained resilience in the NTI, which has declined the first two weeks of January in five of the past six years.

Whether these conditions hold remains to be seen. With the return of a semi-predictable seasonal pattern comes the seasonal decline in spot and outbound tender rejection rates, as late January through February is a slower period in the dry van space. The potential impacts of tariffs remain a wild card. The winner of a glut in imports is a toss-up between full truckload and intermodal, which recently increased its share at the expense of truckload in long-haul corridors like Los Angeles outbound.

The Routing Guide: Links from around the web

DOT releases $320M to repair Helene-damaged truck routes (FreightWaves)

Bay and Bay adds specialized over-dimensional and heavy haul flatbed services (Commercial Carrier Journal)

DOT nominee Duffy vows to prioritize rebuilding I-40 (FreightWaves)

Trucking industry unaffected by restrictions on connected vehicle parts — for now (Trucking Dive)

New entrants are not (completely) crazy

(Fleet Owner)

A different job: trucking isn’t what it used to be

(Commercial Carrier Journal)

The post Analysts predict gradual rate growth amid shifting economic and political winds appeared first on FreightWaves .