Old Dominion Freight Line is fairly hopeful about the new year. It has shouldered the cost burden of carrying more than 30% excess capacity while awaiting a market turn. However, once more volume is poured into the relatively high fixed-cost network, margins will start to meaningfully grow again.

“I’m cautiously optimistic that we’re going to have at least a good second half of 2025, President and CEO Marty Freeman told FreightWaves.

Freeman said he was encouraged by some recent trends, noting that the Institute for Supply Management’s Purchasing Managers’ Index (PMI) moved back into expansion territory in January after 26 months of contraction.

The PMI is a diffusion index measuring sentiment among supply chain managers. A reading above 50 signals growth. The reading for January was 50.9 with the new orders subindex coming in at 55.1. It usually takes a couple of months of positive PMI readings before more volume shows up to LTL carrier networks, but Old Dominion noted some improvement in its industrial business (approximately 55% to 60% of total revenue) on a fourth-quarter call with analysts on Wednesday.

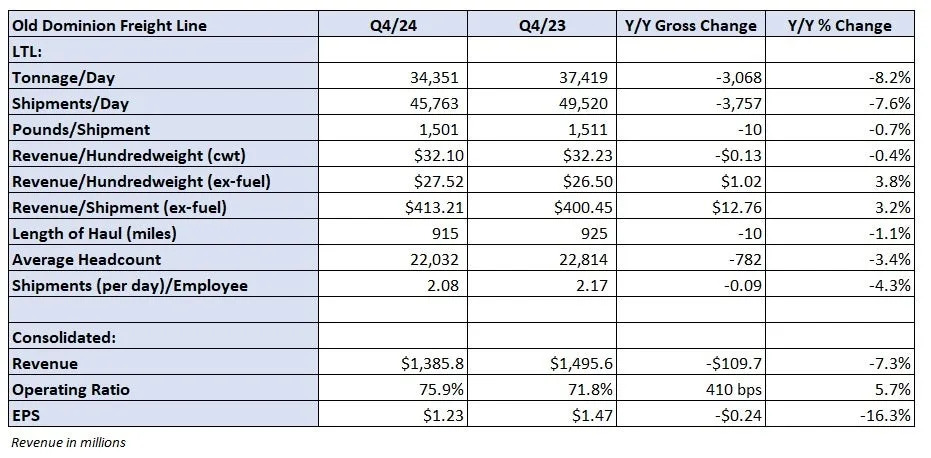

The Thomasville, North Carolina-based less-than-truckload carrier reported earnings per share of $1.23 Wednesday before the market opened, 7 cents higher than the consensus estimate but 24 cents lower year over year. A lower tax rate compared to the year-ago quarter was a 4-cent tailwind in the period.

Revenue fell 7.3% y/y to $1.39 billion in the quarter (down 8.8% on a per-day basis) as tonnage per day declined 8.2% and revenue per hundredweight, or yield, was off 0.4% (3.8% higher excluding fuel surcharges).

The tonnage decline was the combination of a 7.6% decline in daily shipments and a 0.7% dip in weight per shipment. Shipments from Old Dominion’s ( NASDAQ: ODFL ) customers still have fewer pieces with less weight than they did earlier in the cycle – a common theme across the sector.

Demand has yet to meaningfully turn. Tonnage was down 3% from the third to the fourth quarter, which was worse than the normal change rate of negative 1.2%. Approximately 100 basis points of outperformance in December was overshadowed by 100 bps of underperformance in January. The company didn’t quantify the drag that inclement weather had on January but did report that the y/y declines slowed during the month.

Revenue per day was down 4.2% y/y in January, the combination of a 7.1% decline in tonnage and a modest increase in yield (up 4.5% excluding fuel). Management said on the call that it is “still getting good price increases,” noting January yields were slightly better than the normal seasonal trend although a dip in weight per shipment was a contributor to the improved yield metric.

Old Dominion said it has maintained market share throughout the downturn, which it estimates has curtailed volumes by 15% across the industry. It also reminded analysts that it normally takes 600 to 800 bps of market share during upcycles. It added $2 billion in cumulative revenue during the 2021-2022 LTL upswing.

The carrier uses very little third-party capacity, which it sees as a volume opportunity when truckload rates rise as it won’t have to pay up to fulfill linehaul miles like its competitors will.

“When the truckload sector picks up … and their capacity gets tight, they’re going to raise rates on these LTL carriers … whereas we control our own destiny with our own equipment,” Freeman said.

Demand trends over the next two months will have a big impact on how the full year shakes out. Tonnage normally increases 1.5% from January to February and steps 4.9% higher sequentially in March.

Freeman acknowledged some noise around potential changes to U.S. trade policy but said he’s not “overly concerned” about the recent tariff announcements. He expects most of them to get negotiated out as part of broader trade and national security deals. He also said a lower corporate tax rate is very beneficial to Old Dominion’s smaller customers, which will be able to use the money to buy more equipment and produce more goods in-house.

The company forecast revenue to be between $1.34 billion and $1.38 billion in the first quarter, about a 7% y/y decline at the midpoint of the range and 5% lower on a per-day basis. The high end of the range assumes normal seasonality while the low end assumes underperformance like it saw in the fourth quarter. The consensus revenue estimate was $1.4 billion at the time of the print.

The company reported a 75.9% operating ratio (inverse of operating margin) in the quarter, 410 bps worse y/y but in line with prior guidance.

An elevated cost structure from carrying excess door space was again a headwind in the period.

Salaries, wages and benefits expenses (as a percentage of revenue) increased 250 bps y/y. Average head count was down 3.4%, but shipments per employee were off 4.3%.

The company also recorded lower gains on property and equipment sales, and a 100-bp increase in insurance and claims expenses included an annual adjustment to accident claims.

Cost per shipment was up 4.2% y/y while revenue per shipment fell 1.1% – a 530-bp negative spread. The company again expects cost per shipment to stay elevated throughout 2025 (roughly 4% to 4.5% higher).

It normally sees 100 to 150 bps of OR deterioration from the fourth to the first quarter but expects to outperform that change rate this year. The call ranges from no change to a 50-bp increase. That implies a 76.2% OR at the midpoint of the range, 270 bps worse y/y.

The company reiterated a goal of achieving a full-year sub-70% OR in the future.

Old Dominion generated $401 million in cash flow from operations in the quarter ($1.7 billion in 2024).

Full-year 2025 capex guidance of $575 million includes investments of $300 million for real estate projects, $225 million for tractors and trailers, and $50 million for IT. Capex in 2024 equaled $771 million.

The company opened four terminals last year and has several more in the works that will come online when demand dictates the need. Old Dominion currently has 261 terminals in operation.

Shares of ODFL were up 5.4% at 3:43 p.m. EST on Wednesday compared to the S&P 500, which was up 0.2%.

More FreightWaves articles by Todd Maiden:

The post Old Dominion poised to take share when market turns appeared first on FreightWaves .