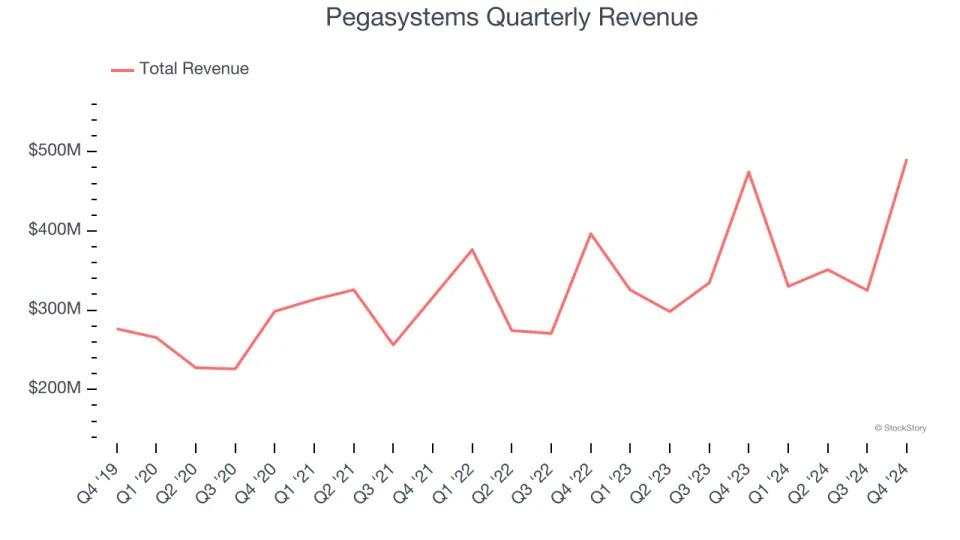

Enterprise workflow software provider Pegasystems (NASDAQ:PEGA) reported Q4 CY2024 results topping the market’s revenue expectations , with sales up 3.5% year on year to $490.8 million. The company’s full-year revenue guidance of $1.6 billion at the midpoint came in 1.1% above analysts’ estimates. Its non-GAAP profit of $1.61 per share was 9.8% above analysts’ consensus estimates.

Is now the time to buy Pegasystems? Find out in our full research report .

Pegasystems (PEGA) Q4 CY2024 Highlights:

Company Overview

Founded by Alan Trefler in 1983, Pegasystems (NASDAQ:PEGA) offers a software-as-a-service platform to automate and optimize workflows in customer service and engagement.

Automation Software

The whole purpose of software is to automate tasks to increase productivity. Today, innovative new software techniques, often involving AI and machine learning, are finally allowing automation that has graduated from simple one- or two-step workflows to more complex processes integral to enterprises. The result is surging demand for modern automation software.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Pegasystems grew its sales at a weak 7.3% compounded annual growth rate. This was below our standard for the software sector and is a poor baseline for our analysis.

This quarter, Pegasystems reported modest year-on-year revenue growth of 3.5% but beat Wall Street’s estimates by 4.4%.

Looking ahead, sell-side analysts expect revenue to grow 5.6% over the next 12 months, a slight deceleration versus the last three years. This projection doesn't excite us and implies its products and services will face some demand challenges.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next .

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

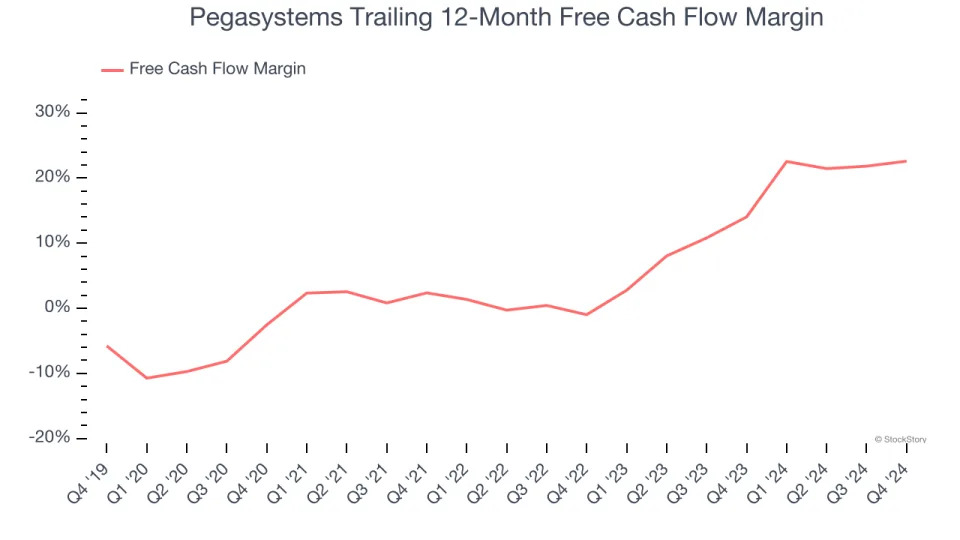

Pegasystems has shown robust cash profitability, driven by its attractive business model and cost-effective customer acquisition strategy that enable it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 22.6% over the last year, quite impressive for a software business.

Pegasystems’s free cash flow clocked in at $92.44 million in Q4, equivalent to a 18.8% margin. This result was good as its margin was 2.5 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts predict Pegasystems’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 22.6% for the last 12 months will increase to 25.1%, giving it more flexibility for investments, share buybacks, and dividends.

Key Takeaways from Pegasystems’s Q4 Results

It was great to see Pegasystems outperform Wall Street’s revenue and EPS estimates this quarter. On the other hand, its full-year EPS guidance missed significantly, causing the stock to trade down 5.1% to $100.61 immediately following the results.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .