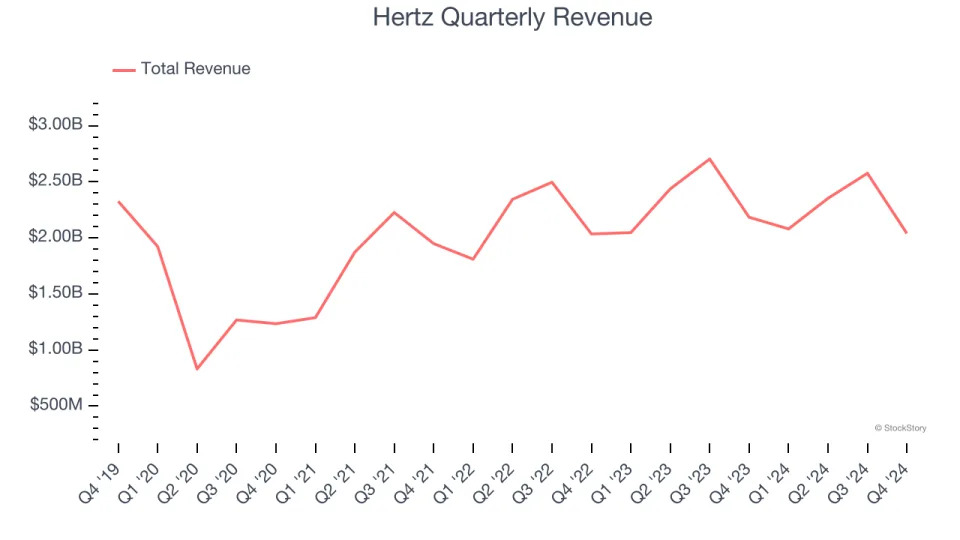

Global car rental company Hertz (NASDAQ:HTZ) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 6.6% year on year to $2.04 billion. Its non-GAAP loss of $1.18 per share was 63.9% below analysts’ consensus estimates.

Is now the time to buy Hertz? Find out in our full research report .

Hertz (HTZ) Q4 CY2024 Highlights:

"Our focus in 2024 was stabilizing the business and implementing fundamental changes to transform our company," said Gil West, Hertz CEO.

Company Overview

Started with a dozen Model T Fords, Hertz (NASDAQ:HTZ) is a global car rental company providing vehicle rental services to leisure and business travelers.

Ground Transportation

The growth of e-commerce and global trade continues to drive demand for shipping services, especially last-mile delivery, presenting opportunities for ground transportation companies. The industry continues to invest in data, analytics, and autonomous fleets to optimize efficiency and find the most cost-effective routes. Despite the essential services this industry provides, ground transportation companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

Sales Growth

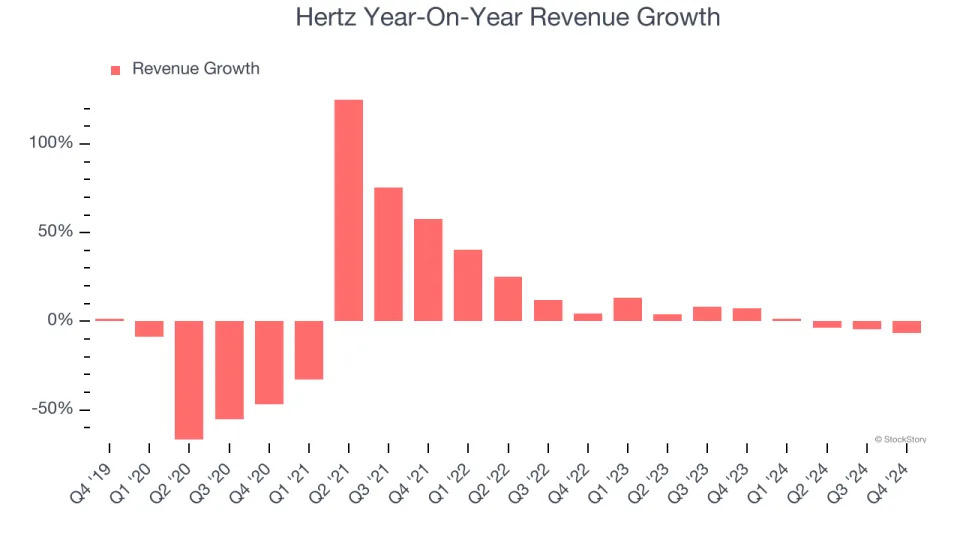

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Hertz struggled to consistently generate demand over the last five years as its sales dropped at a 1.5% annual rate. This fell short of our benchmarks and is a sign of poor business quality.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Hertz’s annualized revenue growth of 2.1% over the last two years is above its five-year trend, but we were still disappointed by the results. We also note many other Ground Transportation businesses have faced declining sales because of cyclical headwinds. While Hertz grew slower than we’d like, it did perform better than its peers.

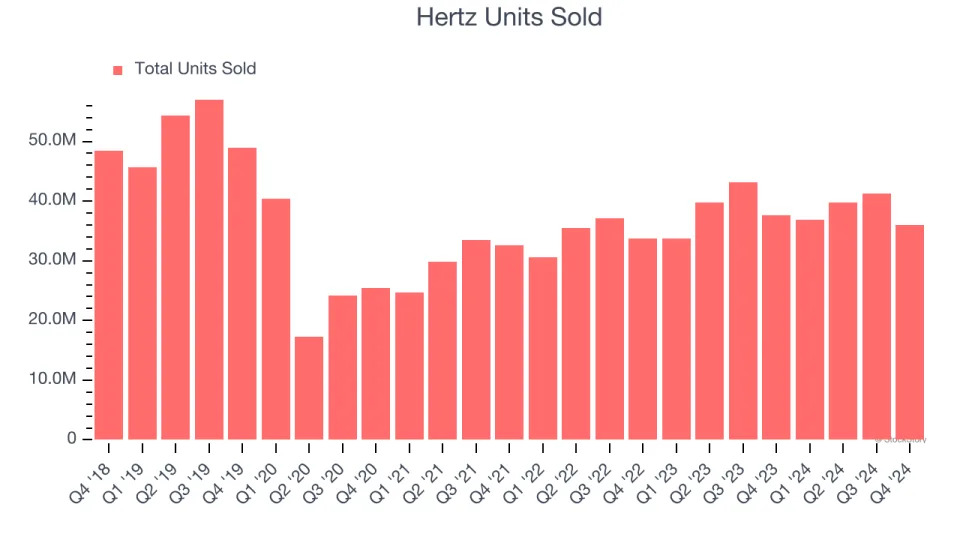

We can dig further into the company’s revenue dynamics by analyzing its units sold, which reached 36 million in the latest quarter. Over the last two years, Hertz’s units sold averaged 6.4% year-on-year growth. Because this number is better than its revenue growth, we can see the company’s average selling price decreased.

This quarter, Hertz missed Wall Street’s estimates and reported a rather uninspiring 6.6% year-on-year revenue decline, generating $2.04 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 1.5% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not catalyze better top-line performance yet.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. .

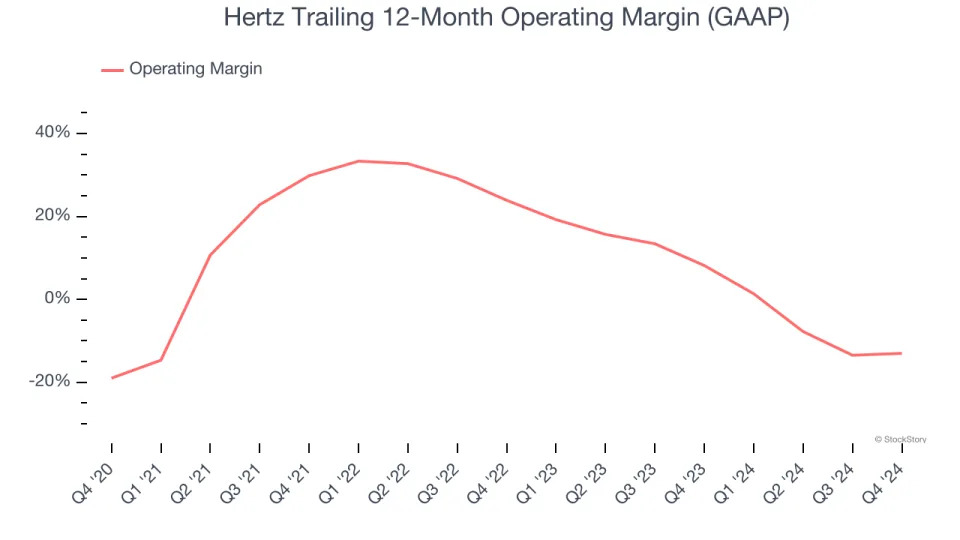

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Hertz was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.2% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Hertz’s operating margin rose by 6 percentage points over the last five years.

This quarter, Hertz generated an operating profit margin of negative 13.1%, up 1.9 percentage points year on year. The increase was encouraging, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

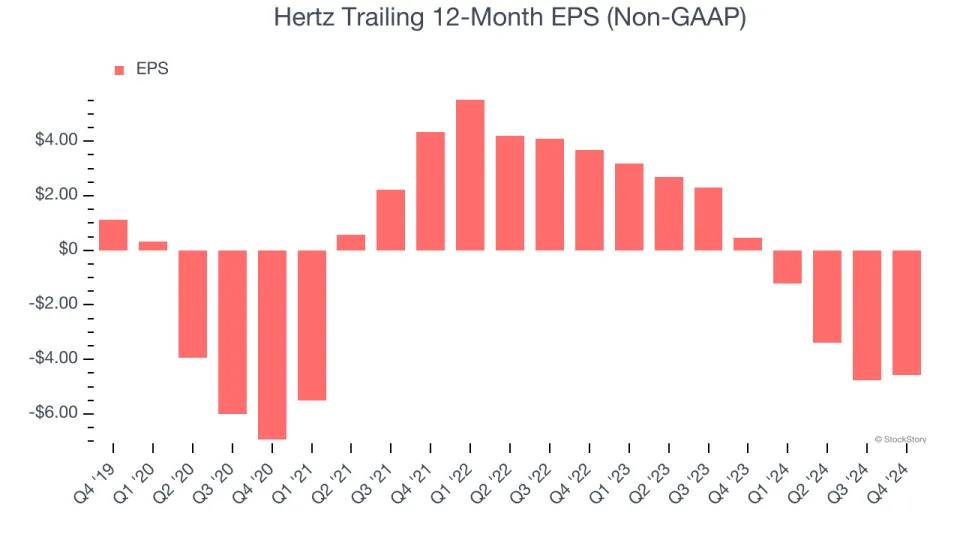

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Hertz, its EPS declined by more than its revenue over the last five years, dropping 43.7% annually. However, its operating margin actually expanded during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

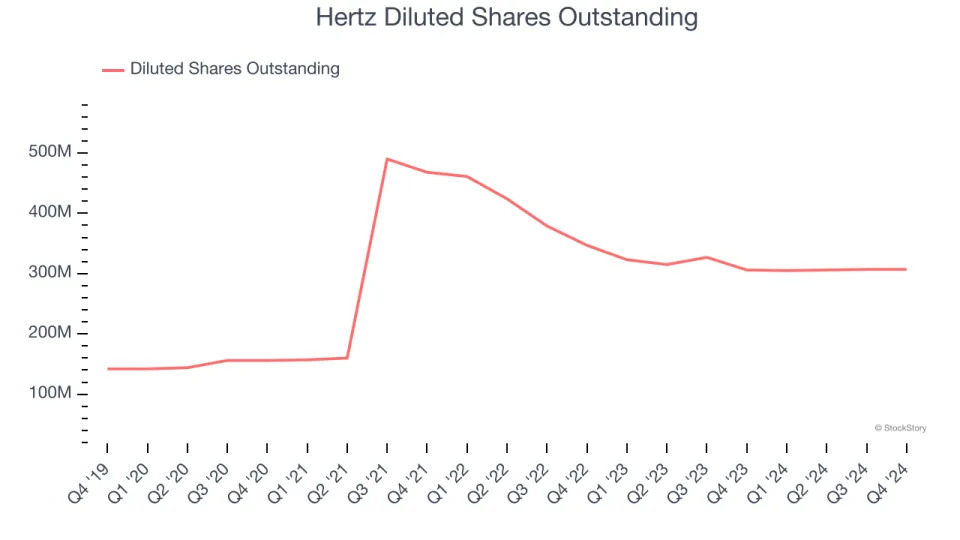

We can take a deeper look into Hertz’s earnings to better understand the drivers of its performance. Hertz recently raised equity capital, and in the process, grew its share count by 116% over the last five years. This has resulted in muted earnings per share growth but doesn’t tell us as much about its future. We prefer to look at operating and free cash flow margins in these situations.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Hertz, its two-year annual EPS declines of 80.2% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Hertz reported EPS at negative $1.18, up from negative $1.36 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Hertz to improve its earnings losses. Analysts forecast its full-year EPS of negative $4.58 will advance to negative $0.92.

Key Takeaways from Hertz’s Q4 Results

We struggled to find many positives in these results as the company missed Wall Street’s estimates across all key metrics. The stock traded down 8.9% to $3.88 immediately after reporting.

Hertz underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free .