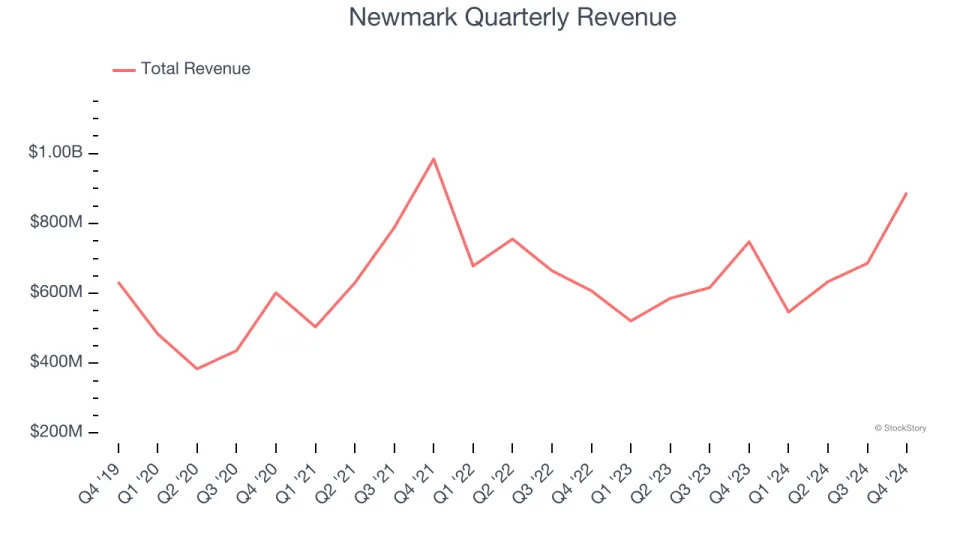

Real estate services firm Newmark (NASDAQ:NMRK) beat Wall Street’s revenue expectations in Q4 CY2024, with sales up 18.8% year on year to $888.3 million. The company expects the full year’s revenue to be around $3 billion, close to analysts’ estimates. Its non-GAAP profit of $0.55 per share was 13.6% above analysts’ consensus estimates.

Is now the time to buy Newmark? Find out in our full research report .

Newmark (NMRK) Q4 CY2024 Highlights:

Company Overview

Founded in 1929, Newmark (NASDAQ:NMRK) provides commercial real estate services, including leasing advisory, global corporate services, investment sales and capital markets, property and facilities management, valuation and advisory, and consulting.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

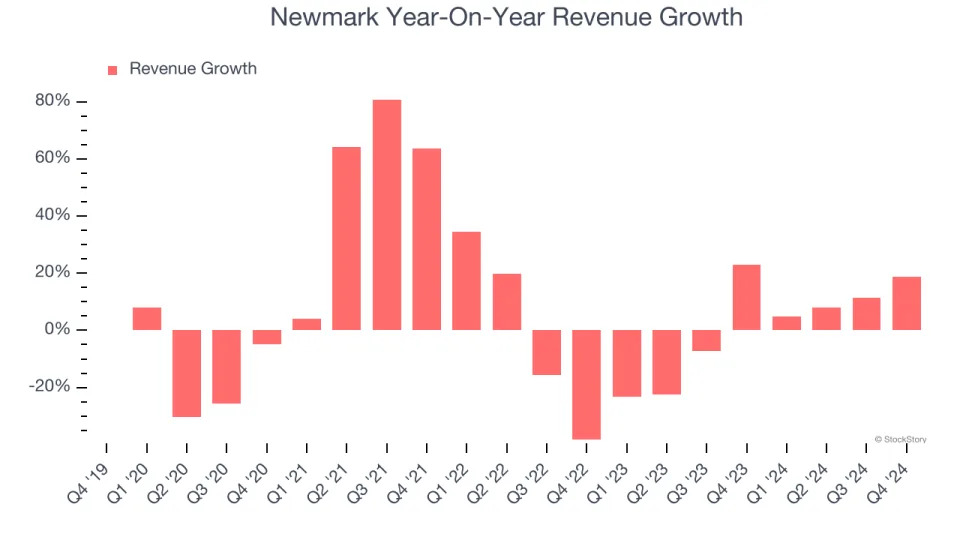

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Newmark’s 4.4% annualized revenue growth over the last five years was sluggish. This was below our standard for the consumer discretionary sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Newmark’s recent history shows its demand slowed as its revenue was flat over the last two years.

Newmark also breaks out the revenue for its three most important segments: Management, Leasing, and Investment Sales, which are 36%, 31%, and 33% of revenue. Over the last two years, Newmark’s revenues in all three segments increased. Its Management revenue (property management) averaged year-on-year growth of 11.3% while its Leasing (sourcing tenants) and Investment Sales (financial advisory) revenues averaged 1.3% and 1.5%.

This quarter, Newmark reported year-on-year revenue growth of 18.8%, and its $888.3 million of revenue exceeded Wall Street’s estimates by 12.3%.

Looking ahead, sell-side analysts expect revenue to grow 8.9% over the next 12 months. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. .

Cash Is King

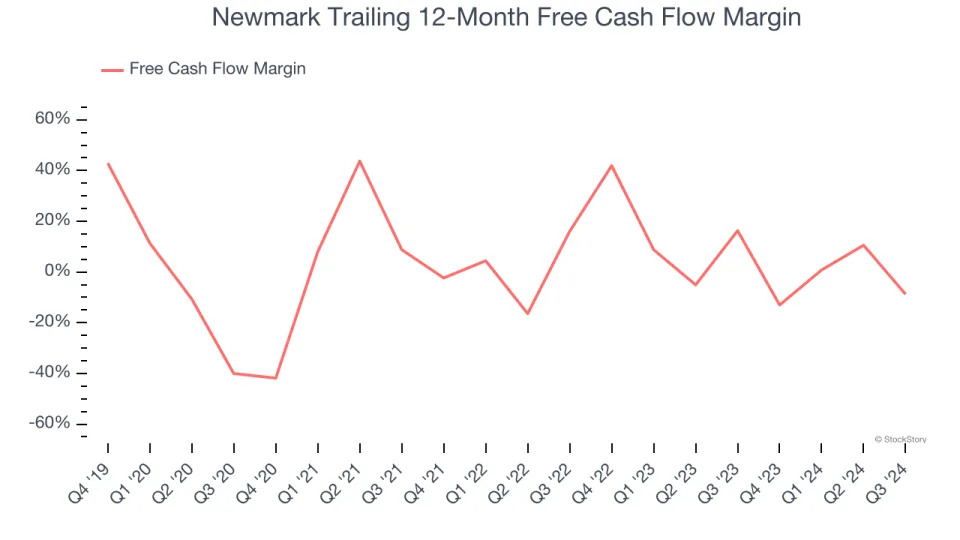

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the last two years, Newmark’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 17.5%, meaning it lit $17.51 of cash on fire for every $100 in revenue.

Key Takeaways from Newmark’s Q4 Results

We were impressed by how significantly Newmark blew past analysts’ revenue expectations this quarter, driven by its Investment Sales division. We were also glad its EPS and EBITDA beat. On the other hand, its full-year EBITDA guidance missed. Still, this quarter had some key positives. The stock traded up 2.6% to $14.20 immediately following the results.

Newmark had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free .