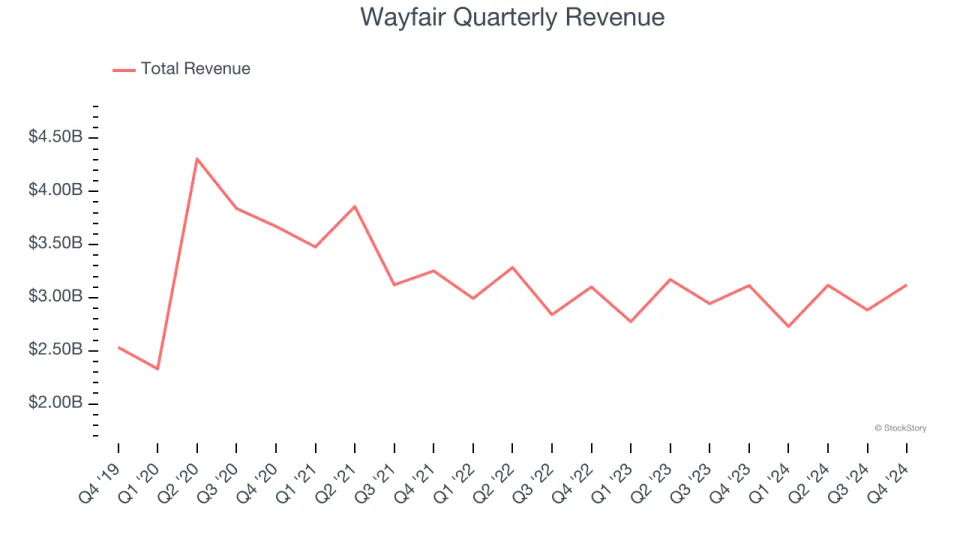

Online home goods retailer Wayfair (NYSE:W) reported Q4 CY2024 results beating Wall Street’s revenue expectations , but sales were flat year on year at $3.12 billion. Its non-GAAP loss of $0.25 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Wayfair? Find out in our full research report .

Wayfair (W) Q4 CY2024 Highlights:

"The fourth quarter was a strong conclusion to the year across multiple fronts. From a topline performance perspective, we ended 2024 on a high note - with net revenue showing positive year-over-year growth. These results enabled us to drive nearly $100 million dollars of adjusted EBITDA in the quarter, and deliver on our goal of approximately 50% year-over-year dollar growth for 2024," said Niraj Shah, CEO, co-founder and co-chairman, Wayfair.

Company Overview

Founded in 2002 by Niraj Shah, Wayfair (NYSE:W) is a leading online retailer of mass-market home goods in the US, UK, Canada, and Germany.

Online Retail

Consumers ever rising demand for convenience, selection, and speed are secular engines underpinning ecommerce adoption. For years prior to Covid, ecommerce penetration as a percentage of overall retail would grow 1-2% annually, but in 2020 adoption accelerated by 5%, reaching 25%, as increased emphasis on convenience drove consumers to structurally buy more online. The surge in buying caused many online retailers to rapidly grow their logistics infrastructures, preparing them for further growth in the years ahead as consumer shopping habits continue to shift online.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Wayfair’s demand was weak over the last three years as its sales fell at a 4.7% annual rate. This was below our standards and signals it’s a low quality business.

This quarter, Wayfair’s $3.12 billion of revenue was flat year on year but beat Wall Street’s estimates by 2%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. .

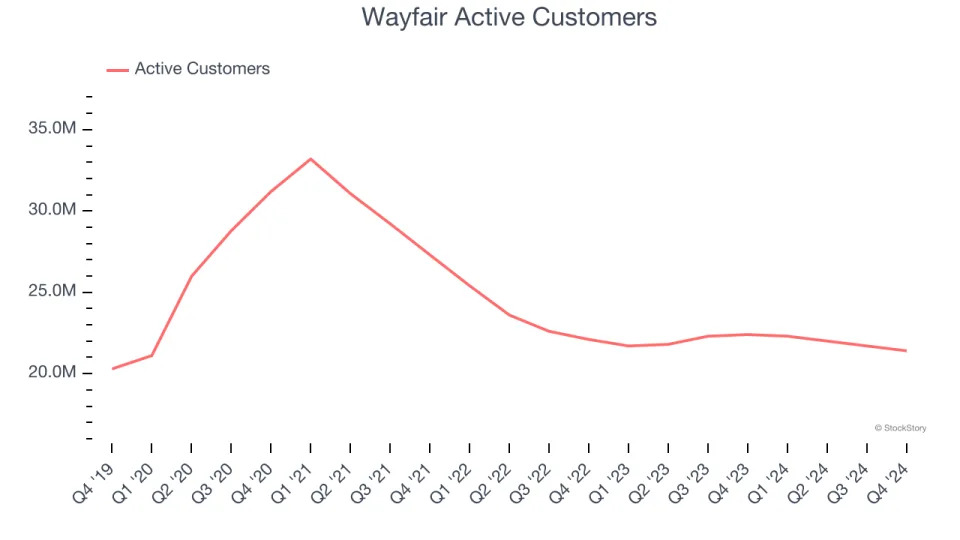

Active Customers

Buyer Growth

As an online retailer, Wayfair generates revenue growth by expanding its number of users and the average order size in dollars.

Wayfair struggled to engage its audience over the last two years as its active customers have declined by 3.2% annually to 21.4 million in the latest quarter. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Wayfair wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

In Q4, Wayfair’s active customers once again decreased by 1 million, a 4.5% drop since last year. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t moving the needle for buyers yet.

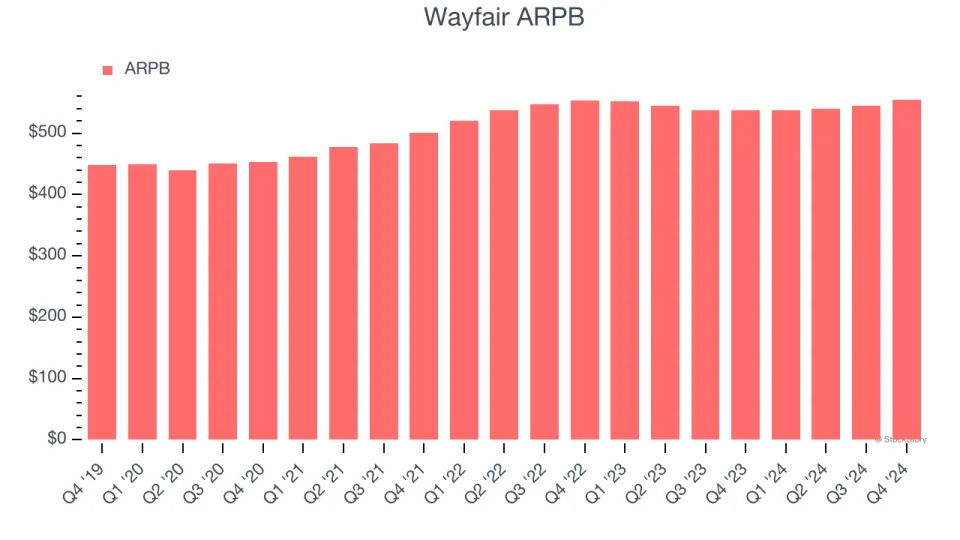

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track for online retailers like Wayfair because it measures how much customers spend per order.

Wayfair’s ARPB has been roughly flat over the last two years. This raises questions about its platform’s health when paired with its declining active customers. If Wayfair wants to increase its buyers, it must either develop new features or provide some existing ones for free.

This quarter, Wayfair’s ARPB clocked in at $555. It grew by 3.4% year on year, faster than its active customers.

Key Takeaways from Wayfair’s Q4 Results

It was encouraging to see Wayfair beat analysts’ revenue expectations this quarter. On the other hand, its number of active customers missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 7.4% to $42.89 immediately following the results.

Wayfair’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free .