Toy and entertainment company Hasbro (NASDAQ:HAS) beat Wall Street’s revenue expectations in Q4 CY2024, but sales fell by 14.5% year on year to $1.10 billion. Its non-GAAP profit of $0.46 per share was 39.3% above analysts’ consensus estimates.

Is now the time to buy Hasbro? Find out in our full research report .

Hasbro (HAS) Q4 CY2024 Highlights:

“I’m proud of our team for delivering what we promised in 2024: we grew in games and licensing, stepped up our operational efficiency, and vastly improved the performance of our toy business,” said Chris Cocks, Hasbro’s Chief Executive Officer.

Company Overview

Credited with the creation of toys such as Mr. Potato Head and the Rubik’s Cube, Hasbro (NASDAQ:HAS) is a global entertainment company offering a diverse range of toys, games, and multimedia experiences for children and families.

Toys and Electronics

The toys and electronics industry presents both opportunities and challenges for investors. Established companies often enjoy strong brand recognition and customer loyalty while smaller players can carve out a niche if they develop a viral, hit new product. The downside, however, is that success can be short-lived because the industry is very competitive: the barriers to entry for developing a new toy are low, which can lead to pricing pressures and reduced profit margins, and the rapid pace of technological advancements necessitates continuous product updates, increasing research and development costs, and shortening product life cycles for electronics companies. Furthermore, these players must navigate various regulatory requirements, especially regarding product safety, which can pose operational challenges and potential legal risks.

Sales Growth

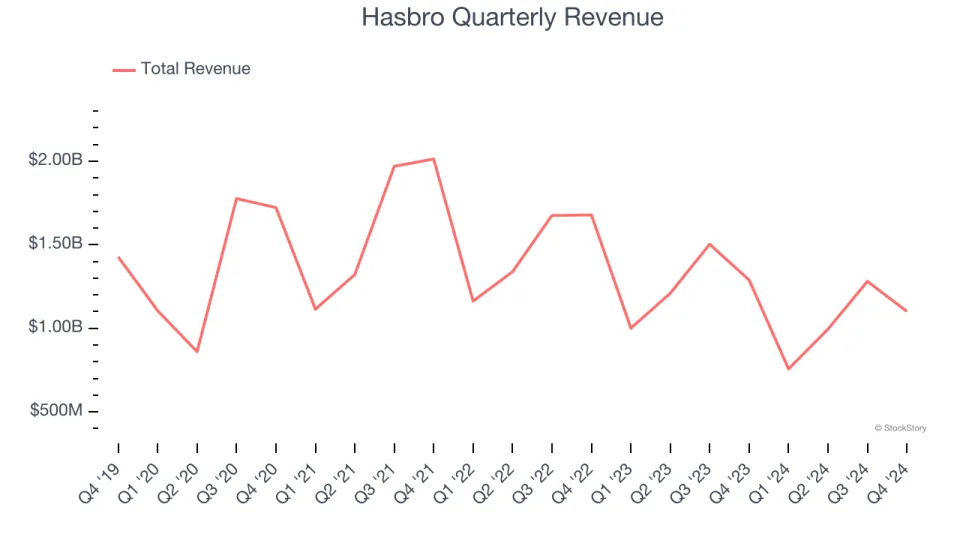

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Hasbro’s demand was weak over the last five years as its sales fell at a 2.6% annual rate. This fell short of our benchmarks and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Hasbro’s recent history shows its demand has stayed suppressed as its revenue has declined by 16% annually over the last two years.

We can better understand the company’s revenue dynamics by analyzing its three most important segments: Consumer Products, Entertainment, and Wizards & Digital Gaming, which are 67.7%, 1.5%, and 30.8% of revenue. Over the last two years, Hasbro’s Consumer Products (toys, games, apparel) and Entertainment (content) revenues averaged year-on-year declines of 16% and 57.9% while its Wizards & Digital Gaming revenue (Wizards of the Coast) averaged 8.1% growth.

This quarter, Hasbro’s revenue fell by 14.5% year on year to $1.10 billion but beat Wall Street’s estimates by 7.6%.

Looking ahead, sell-side analysts expect revenue to grow 2.1% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next .

Cash Is King

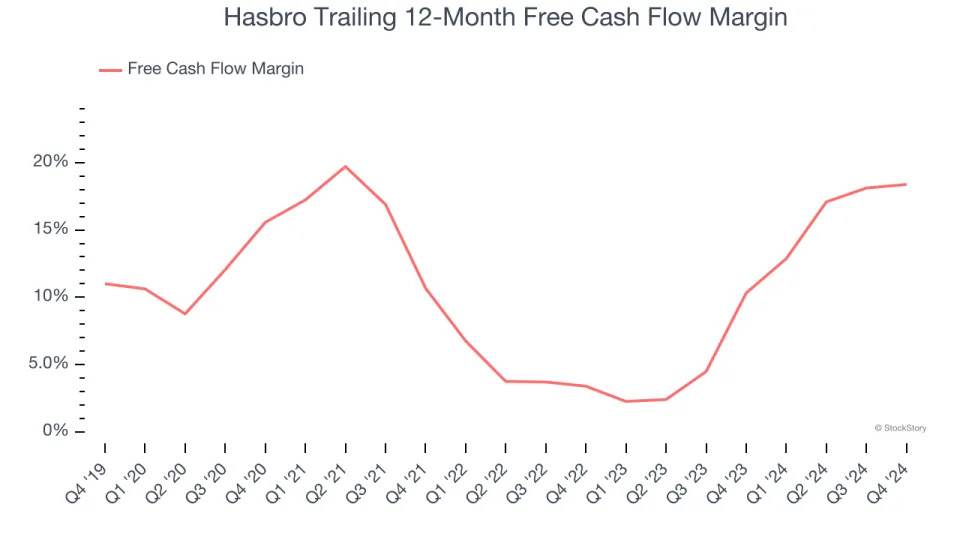

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Hasbro has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 14% over the last two years, better than the broader consumer discretionary sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Hasbro’s free cash flow clocked in at $318.8 million in Q4, equivalent to a 28.9% margin. This result was good as its margin was 2.4 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

Key Takeaways from Hasbro’s Q4 Results

We were impressed by how significantly Hasbro blew past analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a solid quarter. The stock traded up 1.5% to $62 immediately following the results.

Hasbro put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .