Power conversion and control solutions provider Vicor Corporation (NASDAQ:VICR) reported Q4 CY2024 results beating Wall Street’s revenue expectations , with sales up 3.8% year on year to $96.17 million. Its GAAP profit of $0.23 per share was 58.6% above analysts’ consensus estimates.

Is now the time to buy Vicor? Find out in our full research report .

Vicor (VICR) Q4 CY2024 Highlights:

Commenting on fourth quarter performance, Chief Executive Officer Dr. Patrizio Vinciarelli stated: “Revenues and gross margins improved. Further margin improvements depend upon higher utilization of our ChiP fab and increased licensing income. These revenue and income streams are synergistic as our standard license provides royalty discounts commensurate to the Licensee’s annual purchases of Vicor modules. Licensing has been gaining traction with companies whose computing hardware is increasingly dependent on high density power system solutions pioneered and patented by Vicor, including NBMs. Avoiding infringement is the ethical choice, but hyper-scalers also want to avoid the risk of their computing hardware being excluded from importation into the United States. Patent infringement has severe consequences.”

Company Overview

Founded by a researcher at the Massachusetts Institute of Technology, Vicor (NASDAQ:VICR) provides electrical power conversion and delivery products for a range of industries.

Electronic Components

Like many equipment and component manufacturers, electronic components companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include data centers and telecommunications, which can benefit companies whose optical and transceiver offerings fit those markets. But like the broader industrials sector, these companies are also at the whim of economic cycles. Consumer spending, for example, can greatly impact these companies’ volumes.

Sales Growth

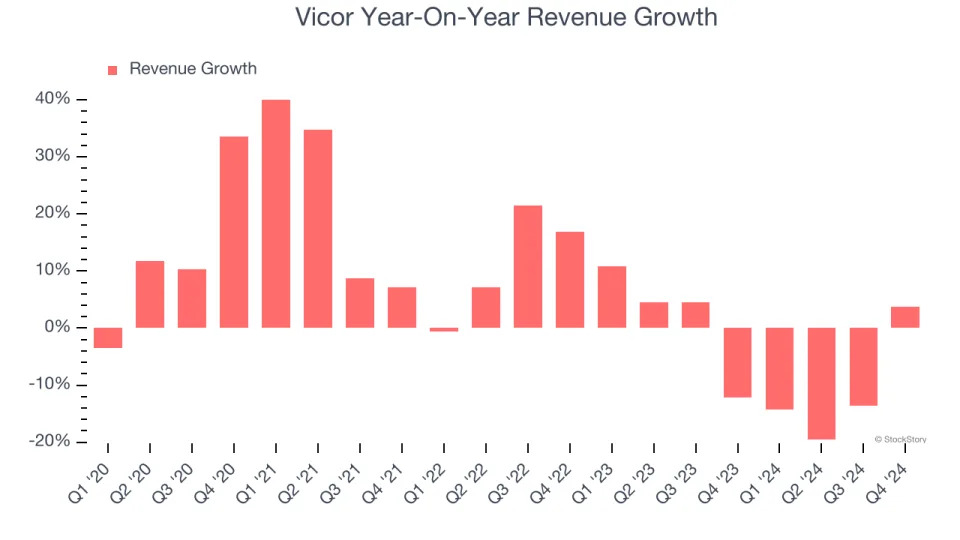

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Vicor’s sales grew at a mediocre 6.4% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Vicor’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5.1% annually. Vicor isn’t alone in its struggles as the Electronic Components industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, Vicor reported modest year-on-year revenue growth of 3.8% but beat Wall Street’s estimates by 5.6%.

Looking ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and indicates its newer products and services will catalyze better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link .

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

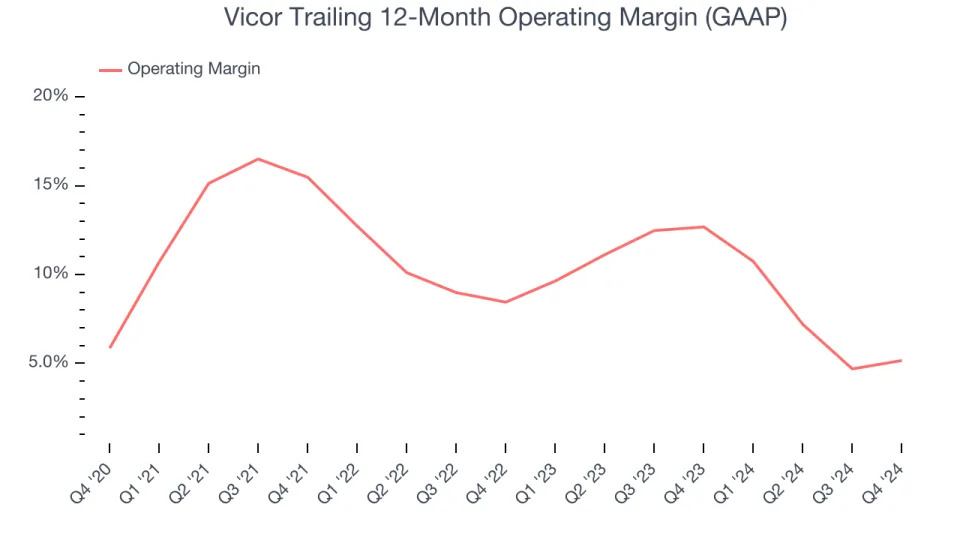

Vicor has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 9.7%, higher than the broader industrials sector.

Looking at the trend in its profitability, Vicor’s operating margin might have seen some fluctuations but has generally stayed the same over the last five years . Shareholders will want to see Vicor grow its margin in the future.

This quarter, Vicor generated an operating profit margin of 9.6%, up 1.6 percentage points year on year. The increase was encouraging, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

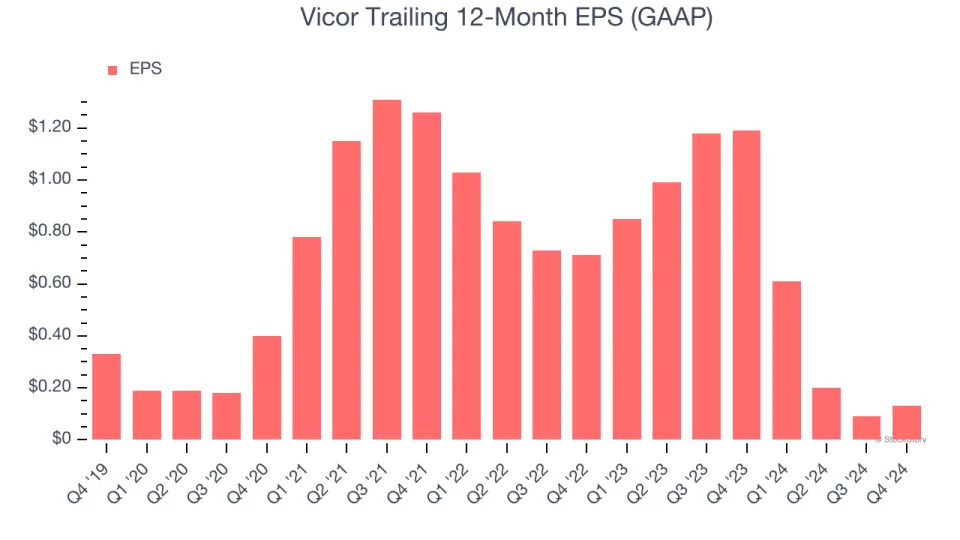

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Vicor, its EPS declined by 17% annually over the last five years while its revenue grew by 6.4%. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

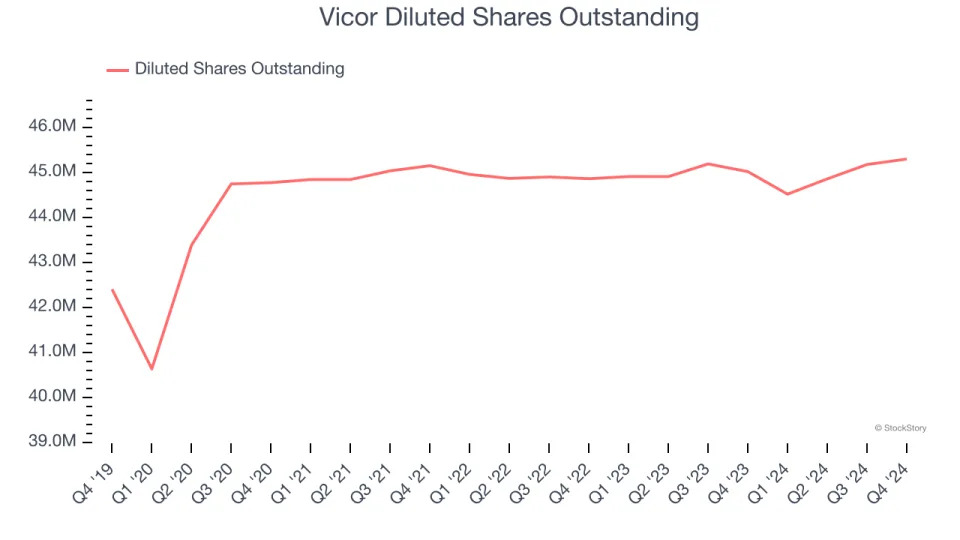

We can take a deeper look into Vicor’s earnings to better understand the drivers of its performance. A five-year view shows Vicor has diluted its shareholders, growing its share count by 6.8%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Vicor, its two-year annual EPS declines of 57.2% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Vicor reported EPS at $0.23, up from $0.19 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Vicor’s full-year EPS of $0.13 to grow 604%.

Key Takeaways from Vicor’s Q4 Results

We were impressed by how significantly Vicor blew past analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid quarter. The stock traded up 3.1% to $53.50 immediately after reporting.

Vicor had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is just one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .