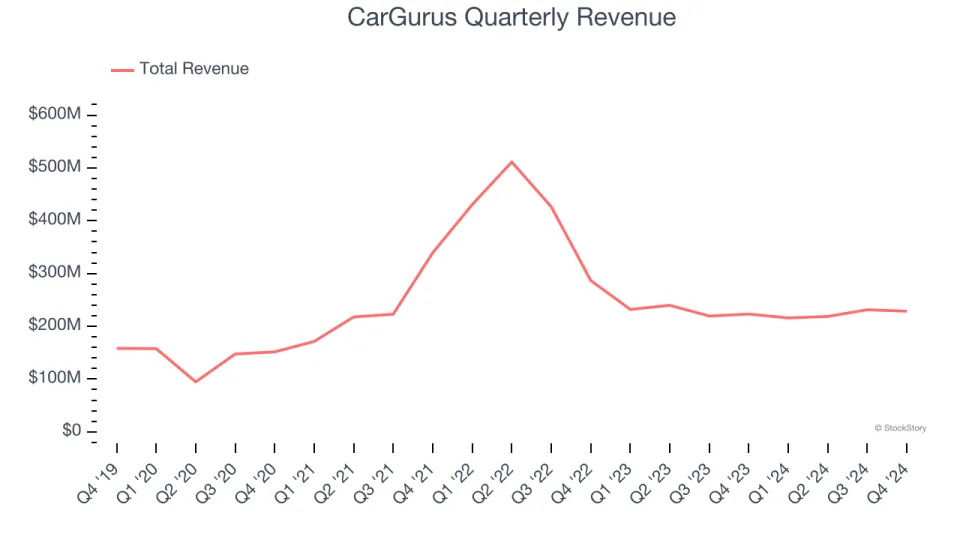

Online auto marketplace CarGurus (NASDAQ:CARG) fell short of the market’s revenue expectations in Q4 CY2024 as sales rose 2.4% year on year to $228.5 million. Next quarter’s revenue guidance of $226 million underwhelmed, coming in 5.2% below analysts’ estimates. Its non-GAAP profit of $0.55 per share was 6.2% above analysts’ consensus estimates.

Is now the time to buy CarGurus? Find out in our full research report .

CarGurus (CARG) Q4 CY2024 Highlights:

“We delivered exceptional results in 2024, with sustained revenue acceleration and significant margin expansion across geographies. Our Marketplace business achieved double-digit growth, driven by continued migration to premium tiers, strong OEM advertising demand, and growing adoption of our value-added products and services," said Jason Trevisan, Chief Executive Officer at CarGurus.

Company Overview

Bringing transparency to a sometimes opaque process, CarGurus (NASDAQ:CARG) is a digital marketplace where auto dealers can connect with potential customers and where car buyers can browse, purchase, and obtain financing.

Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. CarGurus’s demand was weak over the last three years as its sales fell at a 2% annual rate. This fell short of our benchmarks and is a poor baseline for our analysis.

This quarter, CarGurus’s revenue grew by 2.4% year on year to $228.5 million, falling short of Wall Street’s estimates. Company management is currently guiding for a 4.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.5% over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. .

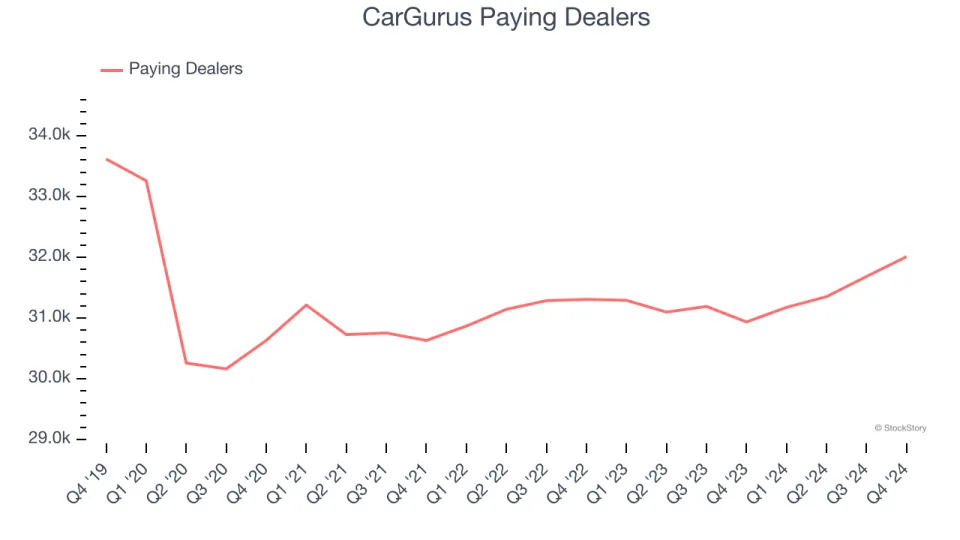

Paying Dealers

User Growth

As an online marketplace, CarGurus generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

CarGurus struggled to engage its audience over the last two years as its paying dealers were flat at 32,010. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If CarGurus wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

Luckily, CarGurus added 1,075 paying dealers in Q4, leading to 3.5% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating user growth.

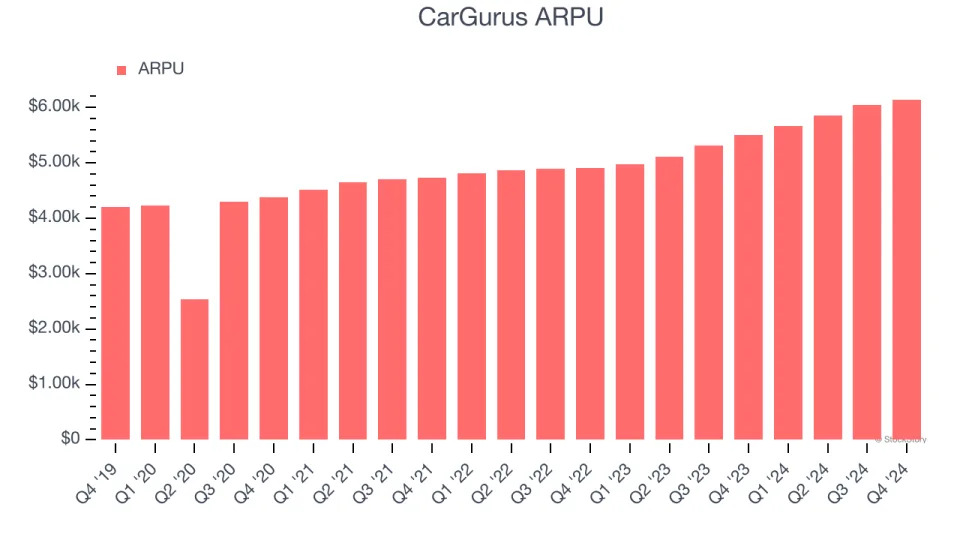

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track for online marketplace businesses like CarGurus because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and CarGurus’s take rate, or "cut", on each order.

CarGurus’s ARPU growth has been exceptional over the last two years, averaging 10.3%. Although its paying dealers were flat during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing users.

This quarter, CarGurus’s ARPU clocked in at $6,144. It grew by 11.6% year on year, faster than its paying dealers.

Key Takeaways from CarGurus’s Q4 Results

It was encouraging to see CarGurus’s EBITDA guidance for next quarter beat analysts’ expectations. We were also happy its EPS and EBITDA outperformed Wall Street’s estimates. On the other hand, its revenue and revenue guidance for next quarter fell short. Overall, this was a softer quarter due to the weaker top-line momentum. The stock traded down 9% to $34.23 immediately after reporting.

CarGurus may have had a tough quarter, but does that actually create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free .