Nextdoor has gotten torched over the last six months - since September 2024, its stock price has dropped 28.5% to $1.71 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Nextdoor, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free .

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons why KIND doesn't excite us and a stock we'd rather own.

Why Is Nextdoor Not Exciting?

Helping residents figure out what's happening on their block in real time, Nextdoor (NYSE:KIND) is a social network that connects neighbors with each other and with local businesses.

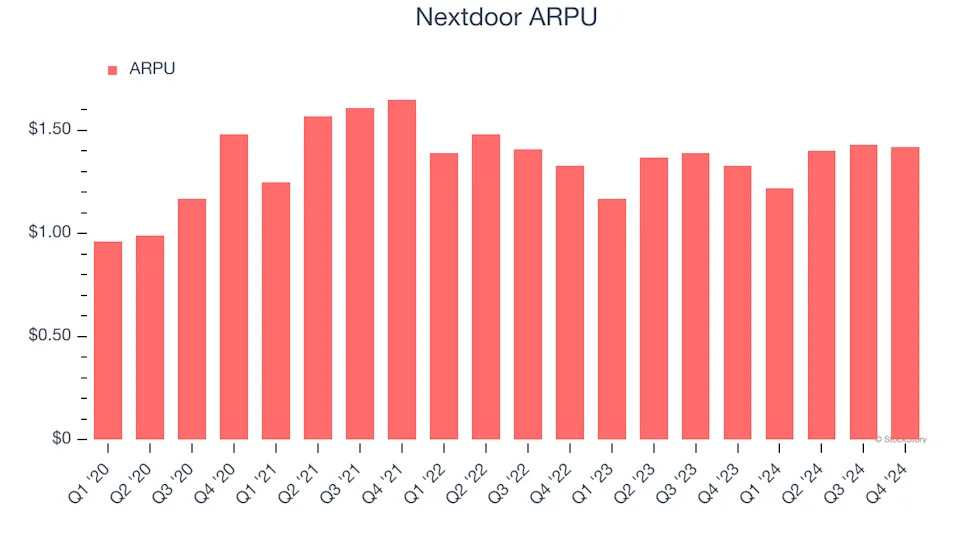

1. Customer Spending Decreases, Engagement Falling?

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Nextdoor’s audience and its ad-targeting capabilities.

Nextdoor’s ARPU fell over the last two years, averaging 1.1% annual declines. This isn’t great, but the increase in weekly active users is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Nextdoor tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

2. Operating Losses Sound the Alarms

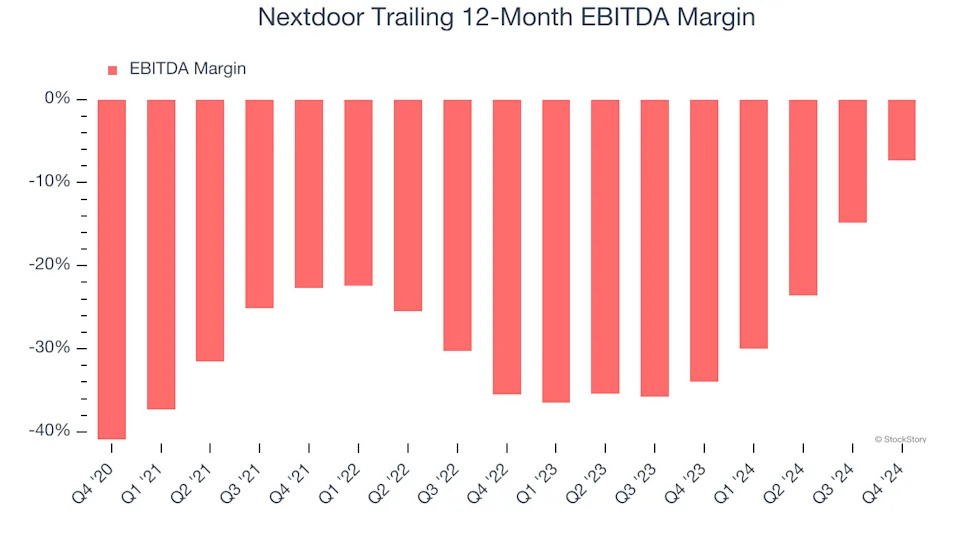

Investors frequently analyze operating income to understand a business’s core profitability. Similar to operating income, EBITDA is a common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of profit potential.

Although Nextdoor was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average EBITDA margin of negative 19.8% over the last two years. Unprofitable consumer internet companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Nextdoor reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

3. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Nextdoor posted positive free cash flow this quarter, the broader story hasn’t been so clean. Nextdoor’s demanding reinvestments have drained its resources over the last two years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 17.2%, meaning it lit $17.21 of cash on fire for every $100 in revenue.

Final Judgment

Nextdoor’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 3.1× forward price-to-gross profit (or $1.71 per share). At this valuation, there’s a lot of good news priced in - you can find better investment opportunities elsewhere. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce .

Stocks We Would Buy Instead of Nextdoor

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free .