According to data from Amberdata in the last month of February, realized volatility on Tuesdays as of writing averaged to 82, which is higher than for all other weekdays. March 2025 is the most volatile month on average since early 2024, and on average displays a volatility of 67.

The volatility comes as Bitcoin fell 30% from its all-time high, and its one-month annualized daily realized volatility approached 70, far exceeding the average 50.

There have been similar spikes in the volatility of Bitcoin in the past. There were extreme swings in March 2024 after Bitcoin reached an all-time high of $73,000.

Further, in August 2024, Bitcoin saw volatile price action as the yen carry trade unwind became apparent, reinforcing the theme of meaningful price action surrounding macroeconomic releases.

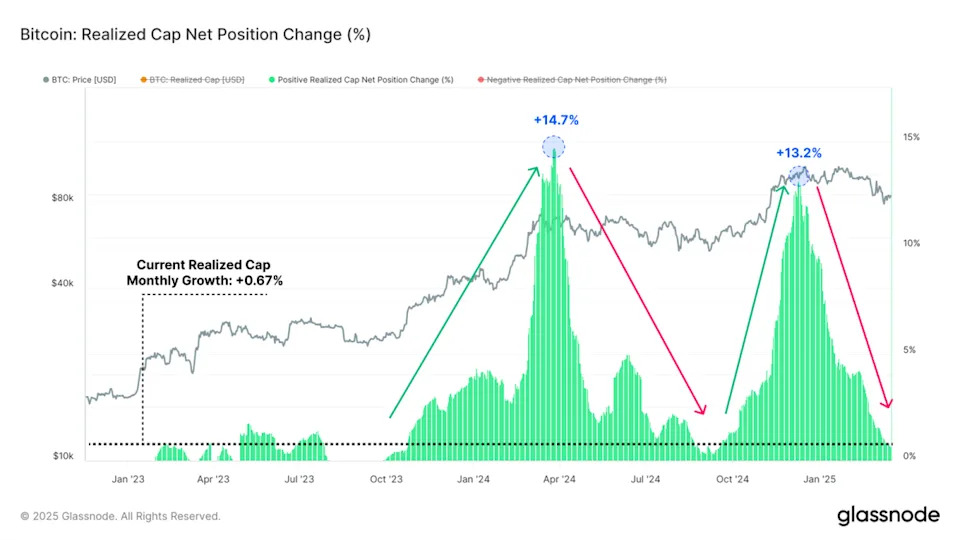

Analyst Ali Martinez believes Bitcoin looks ripe for a bear market according to several metrics. The Inter-Exchange Flow Pulse, a metric that monitors net spot and derivative exchanges orders, rose into a corrective range, suggesting a change in macro trend.

Furthermore, the MVRV Ratio is now negative, indicating that the momentum of Bitcoin has evolved from positive to negative, a historical trend that has told of important turning points in Bitcoin price trends.

Martinez points out that critical support areas exist between $66,000 and $69,000, and he says Bitcoin’s next big move will hinge on if these levels hold or break.

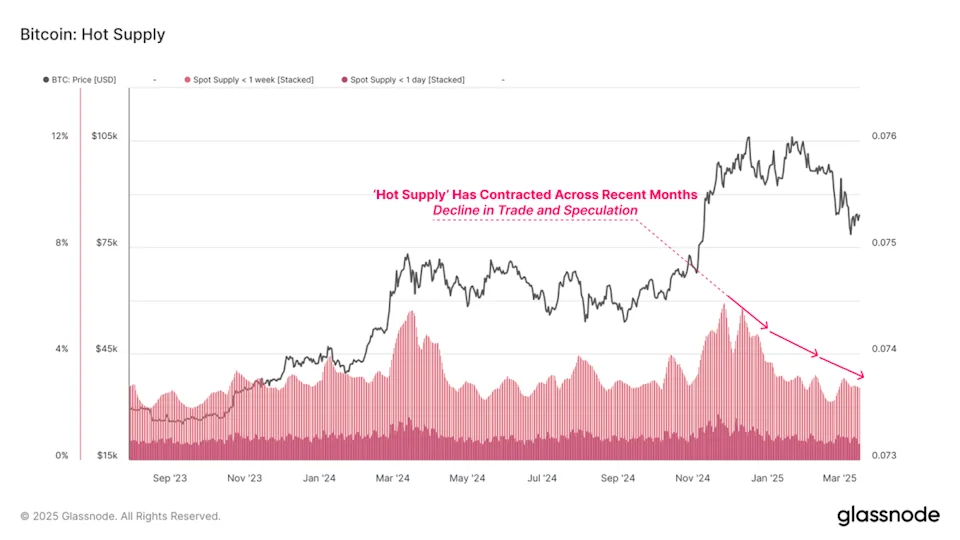

Additionally, Glassnode reports that Bitcoin's "hot supply" — coins held for less than a week — has decreased in the last few months, suggesting less short-term trading and speculation. This indicates that investors are moving toward holding BTC longer, which would likely signal a shift in market sentiment toward a more cautious or long-term-oriented outlook.

With changes in Bitcoin’s market structure, studying daily-specific volatility trends may be essential for guiding investor behavior and determining market participation approaches.