Women’s plus-size apparel retailer Torrid Holdings (NYSE:CURV) reported Q4 CY2024 results beating Wall Street’s revenue expectations , but sales fell by 6.1% year on year to $275.6 million. On the other hand, next quarter’s revenue guidance of $269 million was less impressive, coming in 3% below analysts’ estimates. Its GAAP loss of $0.03 per share was 60% above analysts’ consensus estimates.

Is now the time to buy Torrid? Find out in our full research report .

Torrid (CURV) Q4 CY2024 Highlights:

Lisa Harper, Chief Executive Officer, stated, “We successfully closed fiscal 2024 with positive results, fueled by product innovation in our core assortment and strong customer response to the launch of our high-growth, higher margin sub-brands. Thoughtful growth of our well received sub-brands set the stage for elevated, new and younger customer engagement, incremental lifestyle purchases, as well as creating a halo effect across the business. Combining our successful sub-brand assortment initiatives with our commitment to modernizing and evolving our core Torrid offerings gives me great confidence in the long-term health and growth prospects of our business."

Company Overview

Promoting a message of body positivity and inclusiveness, Torrid Holdings (NYSE:CURV) is a plus-size women’s apparel and accessories retailer.

Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.10 billion in revenue over the past 12 months, Torrid is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

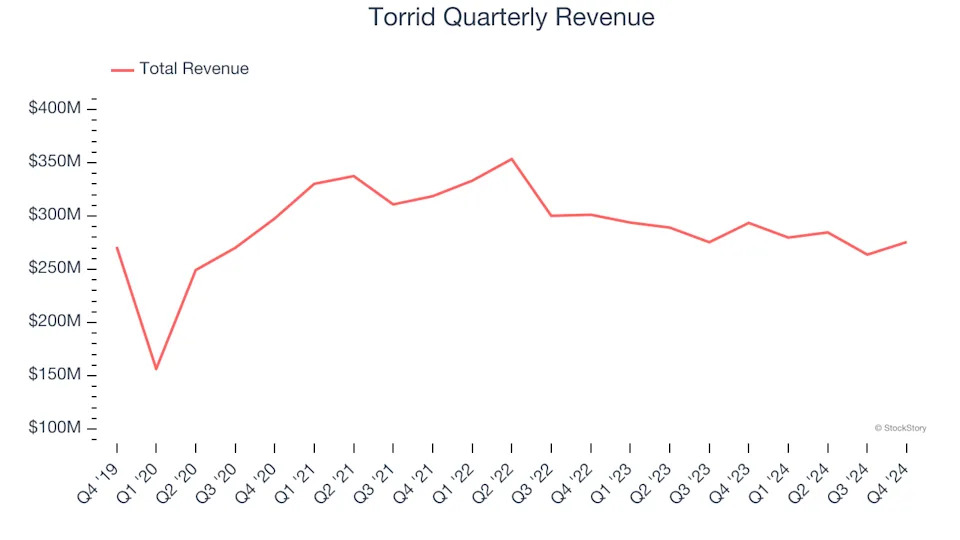

As you can see below, Torrid’s sales grew at a sluggish 1.3% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts).

This quarter, Torrid’s revenue fell by 6.1% year on year to $275.6 million but beat Wall Street’s estimates by 4.2%. Company management is currently guiding for a 3.8% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last five years. This projection is underwhelming and suggests its products will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. .

Store Performance

Number of Stores

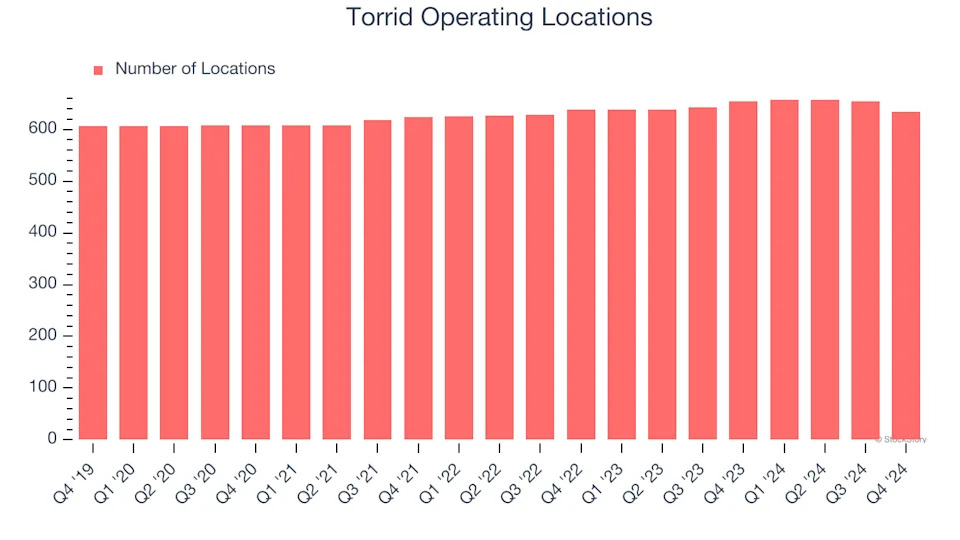

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Torrid operated 634 locations in the latest quarter. It has opened new stores quickly over the last two years, averaging 1.7% annual growth, faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Torrid’s demand has been shrinking over the last two years as its same-store sales have averaged 8.3% annual declines. This performance is concerning - it shows Torrid artificially boosts its revenue by building new stores. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its store base.

In the latest quarter, Torrid’s year on year same-store sales were flat. This performance was a well-appreciated turnaround from its historical levels, showing the business is improving.

Key Takeaways from Torrid’s Q4 Results

We were impressed by how significantly Torrid blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. On the other hand, its full-year revenue and EBITDA guidance missed significantly, and its gross margin fell short of Wall Street’s estimates. Overall, this quarter was mixed but still had some key positives. The stock traded up 5.7% to $5.89 immediately after reporting.

Big picture, is Torrid a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free .