Shareholders of Cars.com would probably like to forget the past six months even happened. The stock dropped 31.7% and now trades at $12.09. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Cars.com, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free .

Despite the more favorable entry price, we're swiping left on Cars.com for now. Here are three reasons why there are better opportunities than CARS and a stock we'd rather own.

Why Is Cars.com Not Exciting?

Originally started as a joint venture between several media companies including The Washington Post and The New York Times, Cars.com (NYSE:CARS) is a digital marketplace that connects new and used car buyers and sellers.

1. Dealer Customers Hit a Plateau

As an online marketplace, Cars.com generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Cars.com struggled with new customer acquisition over the last two years as its dealer customers were flat at 19,206. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Cars.com wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Cars.com’s revenue to rise by 3.3%, a slight deceleration versus its 4.9% annualized growth for the past three years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

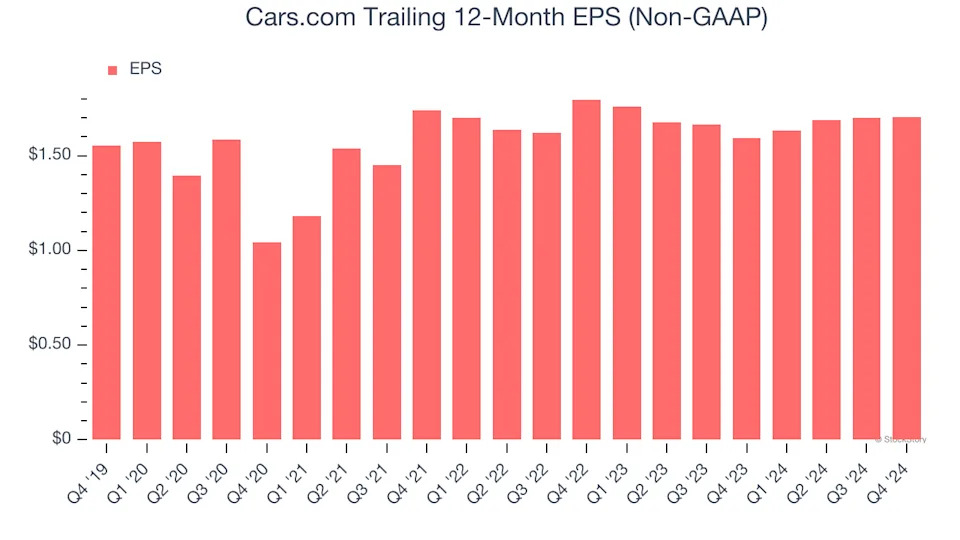

3. EPS Growth Has Stalled

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Cars.com’s flat EPS over the last three years was below its 4.9% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Cars.com isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 3.4× forward EV-to-EBITDA (or $12.09 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of our top digital advertising picks .

Stocks We Like More Than Cars.com

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free .