Wrapping up Q4 earnings, we look at the numbers and key takeaways for the drug development inputs & services stocks, including Medpace (NASDAQ:MEDP) and its peers.

Companies specializing in drug development inputs and services play a crucial role in the pharmaceutical and biotechnology value chain. Essential support for drug discovery, preclinical testing, and manufacturing means stable demand, as pharmaceutical companies often outsource non-core functions with medium to long-term contracts. However, the business model faces high capital requirements, customer concentration, and vulnerability to shifts in biopharma R&D budgets or regulatory frameworks. Looking ahead, the industry will likely enjoy tailwinds such as increasing investment in biologics, cell and gene therapies, and advancements in precision medicine, which drive demand for sophisticated tools and services. There is a growing trend of outsourcing in drug development for nimbleness and cost efficiency, which benefits the industry. On the flip side, potential headwinds include pricing pressures as efforts to contain healthcare costs are always top of mind. An evolving regulatory backdrop could also slow innovation or client activity.

The 8 drug development inputs & services stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 0.8%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 16.2% since the latest earnings results.

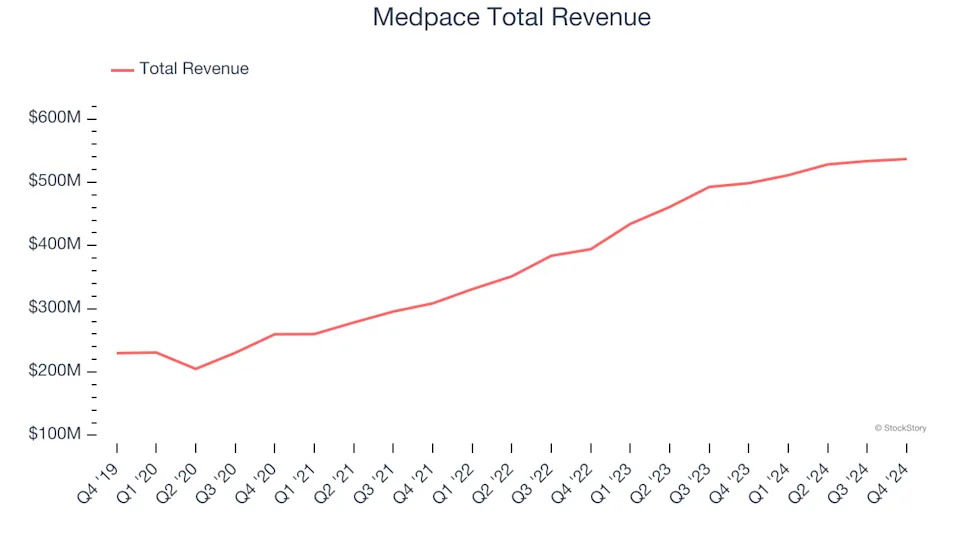

Medpace (NASDAQ:MEDP)

Founded in 1992 as a scientifically-driven alternative to traditional contract research organizations, Medpace (NASDAQ:MEDP) provides outsourced clinical trial management and research services to help pharmaceutical, biotechnology, and medical device companies develop new treatments.

Medpace reported revenues of $536.6 million, up 7.7% year on year. This print was in line with analysts’ expectations, but overall, it was a slower quarter for the company with full-year revenue guidance missing analysts’ expectations.

The stock is down 10% since reporting and currently trades at $318.48.

Is now the time to buy Medpace? Access our full analysis of the earnings results here, it’s free .

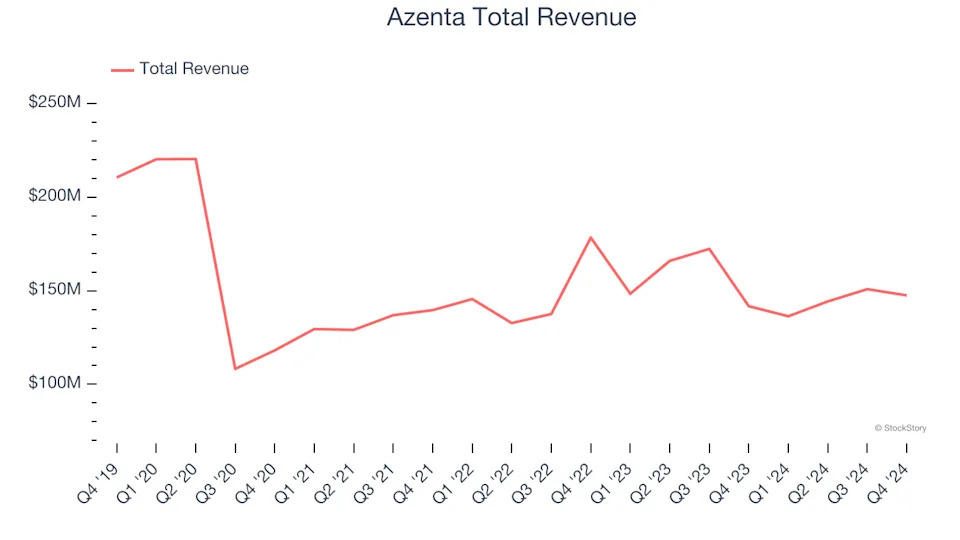

Best Q4: Azenta (NASDAQ:AZTA)

Serving as the guardian of some of medicine's most valuable materials, Azenta (NASDAQ:AZTA) provides biological sample management, storage, and genomic services that help pharmaceutical and biotechnology companies preserve and analyze critical research materials.

Azenta reported revenues of $147.5 million, up 4.1% year on year, outperforming analysts’ expectations by 1.1%. The business had a very strong quarter with a solid beat of analysts’ EPS estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 29.6% since reporting. It currently trades at $36.61.

Is now the time to buy Azenta? Access our full analysis of the earnings results here, it’s free .

Weakest Q4: Fortrea (NASDAQ:FTRE)

Spun off from Labcorp in 2023 to focus exclusively on clinical research services, Fortrea (NASDAQ:FTRE) is a contract research organization that helps pharmaceutical, biotech, and medical device companies develop and bring their products to market through clinical trials and support services.

Fortrea reported revenues of $697 million, down 1.8% year on year, falling short of analysts’ expectations by 0.9%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations.

Fortrea delivered the weakest performance against analyst estimates, slowest revenue growth, and weakest full-year guidance update in the group. As expected, the stock is down 36.5% since the results and currently trades at $8.80.

Read our full analysis of Fortrea’s results here.

Charles River Laboratories (NYSE:CRL)

Named after the Massachusetts river where it was founded in 1947, Charles River Laboratories (NYSE:CRL) provides non-clinical drug development services, research models, and manufacturing support to pharmaceutical and biotechnology companies.

Charles River Laboratories reported revenues of $1.00 billion, down 1.1% year on year. This result topped analysts’ expectations by 2.3%. Taking a step back, it was a mixed quarter as it also produced an impressive beat of analysts’ organic revenue estimates but a miss of analysts’ full-year EPS guidance estimates.

Charles River Laboratories scored the biggest analyst estimates beat among its peers. The stock is up 5.1% since reporting and currently trades at $162.19.

Read our full, actionable report on Charles River Laboratories here, it’s free.

Repligen (NASDAQ:RGEN)

With over 13 strategic acquisitions since 2012 to build its comprehensive bioprocessing portfolio, Repligen (NASDAQ:RGEN) develops and manufactures specialized technologies that improve the efficiency and flexibility of biological drug manufacturing processes.

Repligen reported revenues of $167.5 million, flat year on year. This print was in line with analysts’ expectations. Overall, it was a satisfactory quarter as it also put up a solid beat of analysts’ organic revenue estimates.

Repligen pulled off the highest full-year guidance raise among its peers. The stock is down 7.7% since reporting and currently trades at $139.20.

Read our full, actionable report on Repligen here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here .