Titan International trades at $6.51 per share and has stayed right on track with the overall market, losing 10.5% over the last six months while the S&P 500 is down 11%. This might have investors contemplating their next move.

Is now the time to buy Titan International, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free .

Despite the more favorable entry price, we're cautious about Titan International. Here are three reasons why there are better opportunities than TWI and a stock we'd rather own.

Why Do We Think Titan International Will Underperform?

Acquiring Goodyear’s farm tire business in 2005, Titan (NSYE:TWI) is a manufacturer and supplier of wheels, tires, and undercarriages used in off-highway vehicles such as construction vehicles.

1. Long-Term Revenue Growth Disappoints

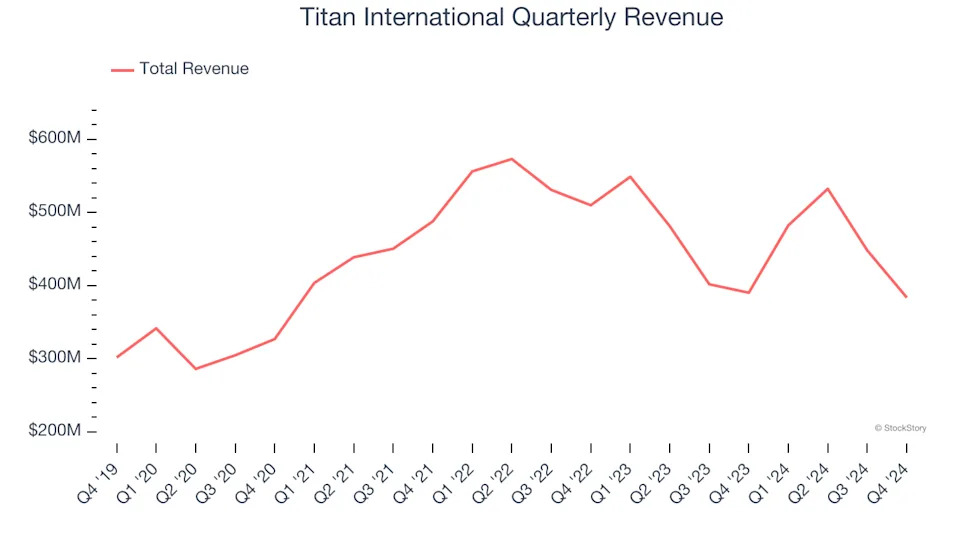

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Titan International’s sales grew at a tepid 5% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector.

2. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

Titan International has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 14% gross margin over the last five years. Said differently, Titan International had to pay a chunky $86.00 to its suppliers for every $100 in revenue.

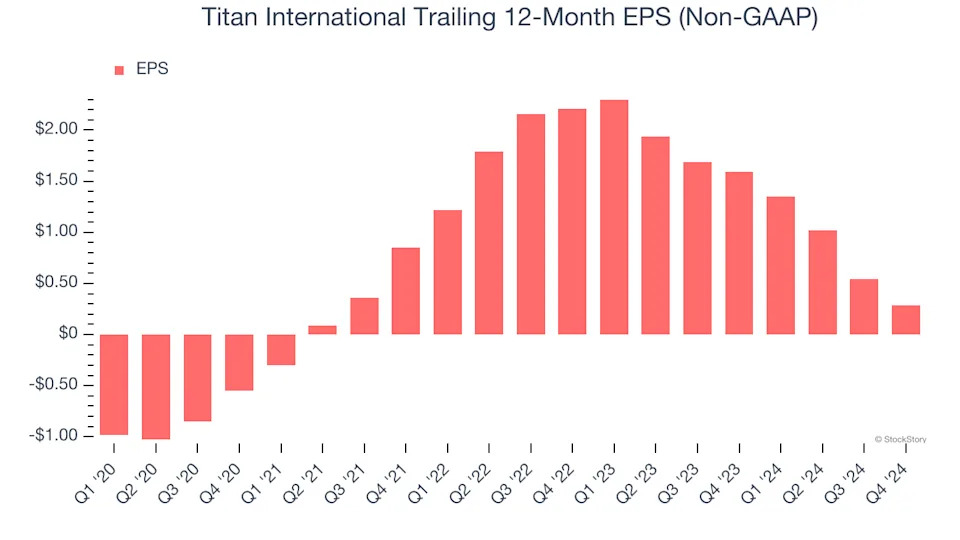

3. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Titan International, its EPS declined by more than its revenue over the last two years, dropping 63.8%. This tells us the company struggled to adjust to shrinking demand.

Final Judgment

We cheer for all companies making their customers lives easier, but in the case of Titan International, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 43.4× forward price-to-earnings (or $6.51 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d recommend looking at our favorite semiconductor picks and shovels play .

Stocks We Like More Than Titan International

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Strong Momentum Stocks for this week . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free .