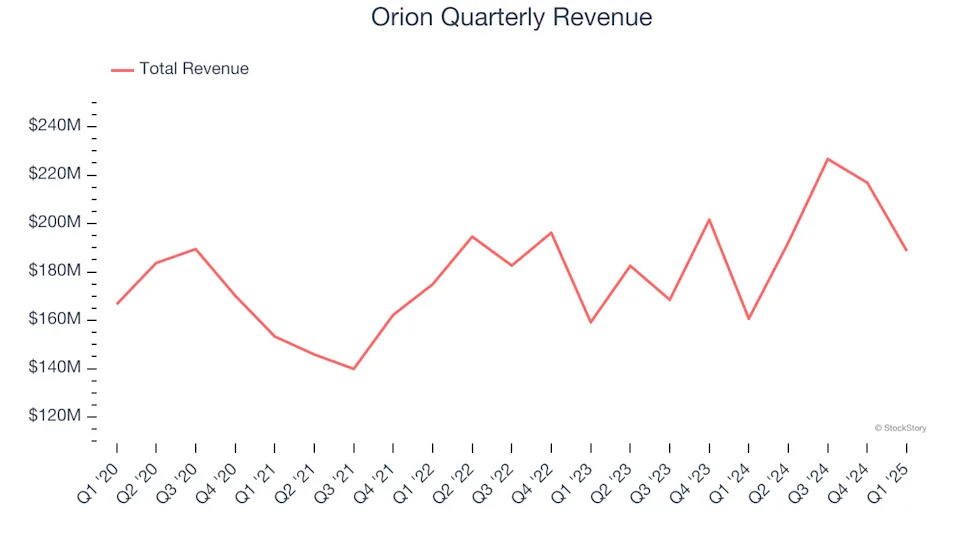

Marine infrastructure company Orion (NYSE:ORN) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, with sales up 17.4% year on year to $188.7 million. The company’s full-year revenue guidance of $825 million at the midpoint came in 1.5% above analysts’ estimates. Its non-GAAP profit of $0.01 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Orion? Find out in our full research report .

Orion (ORN) Q1 CY2025 Highlights:

“We’re off to a strong start in 2025. On a year-over-year basis, our first quarter revenue increased 17% to $189 million and Adjusted EBITDA doubled. This performance reflects the strength of our operating model and the successful execution of our strategic priorities,” said Travis Boone, Chief Executive Officer of Orion Group Holdings.

Company Overview

Established in 1994, Orion (NYSE:ORN) provides construction services for marine infrastructure and industrial projects.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Orion’s 2.4% annualized revenue growth over the last five years was sluggish. This was below our standards and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Orion’s annualized revenue growth of 6.1% over the last two years is above its five-year trend, but we were still disappointed by the results.

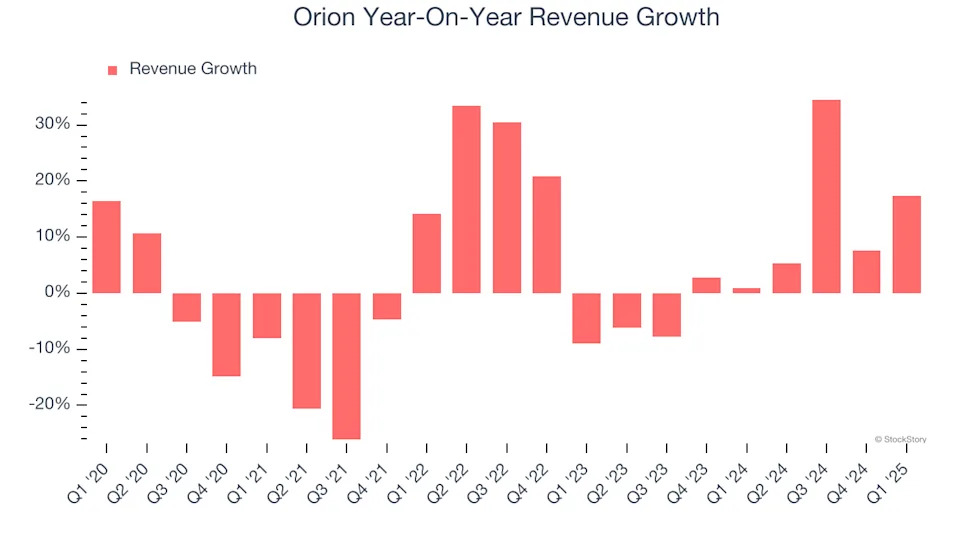

This quarter, Orion reported year-on-year revenue growth of 17.4%, and its $188.7 million of revenue exceeded Wall Street’s estimates by 8.8%.

Looking ahead, sell-side analysts expect revenue to grow 1.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. .

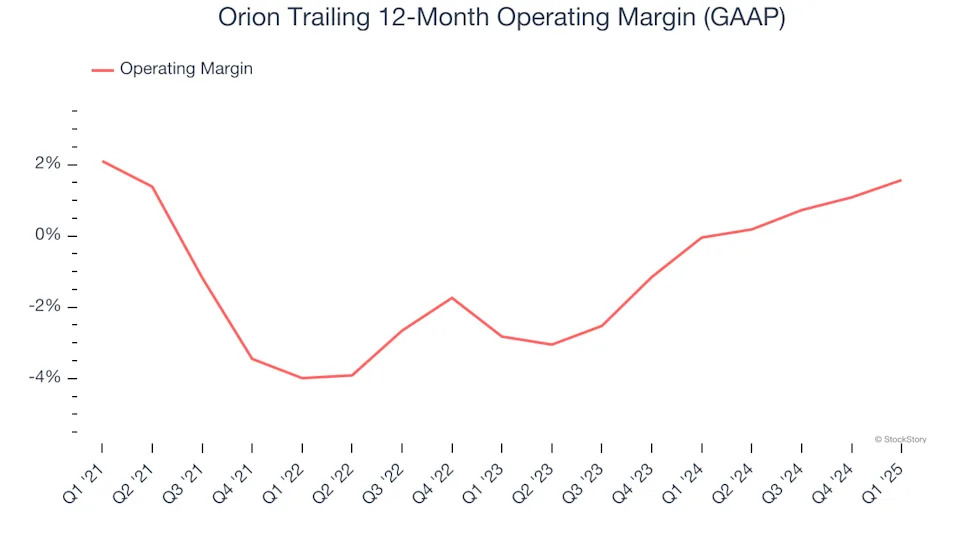

Operating Margin

Orion was roughly breakeven when averaging the last five years of quarterly operating profits, one of the worst outcomes in the industrials sector. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Orion’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Orion’s breakeven margin was up 2.6 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

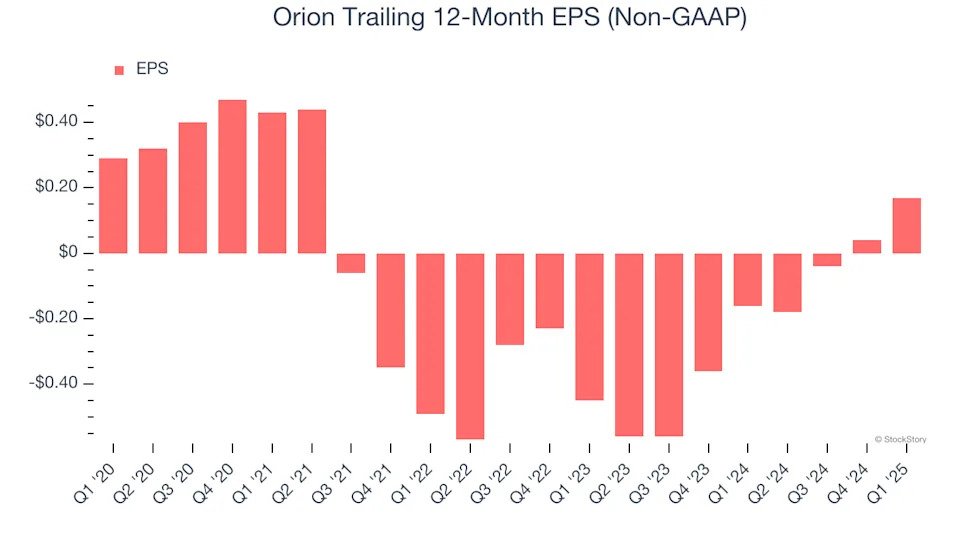

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Orion, its EPS declined by 10.1% annually over the last five years while its revenue grew by 2.4%. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

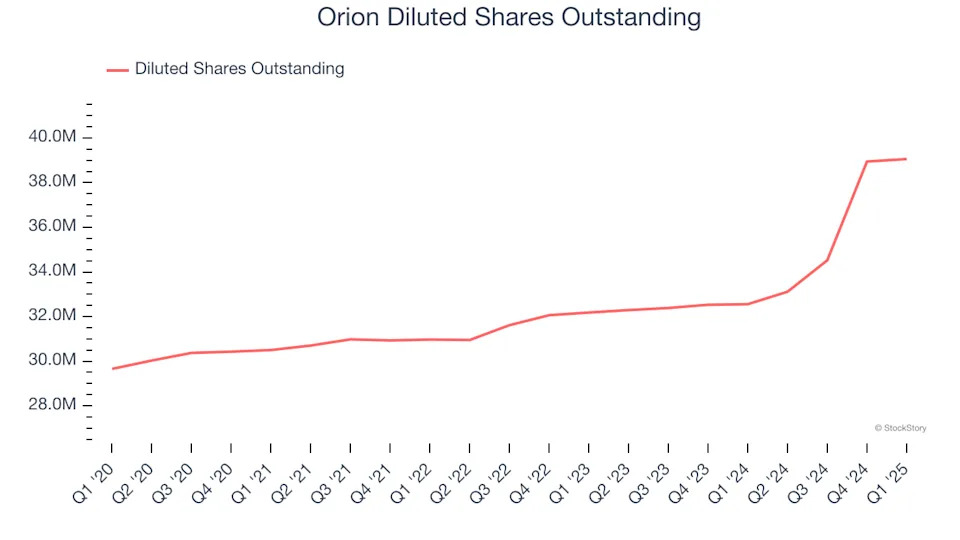

We can take a deeper look into Orion’s earnings to better understand the drivers of its performance. A five-year view shows Orion has diluted its shareholders, growing its share count by 31.7%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Orion, its two-year annual EPS growth of 54.2% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q1, Orion reported EPS at $0.01, up from negative $0.12 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Orion to perform poorly. Analysts forecast its full-year EPS of $0.17 will hit $0.16.

Key Takeaways from Orion’s Q1 Results

We were impressed by how significantly Orion blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also excited its full-year EBITDA guidance topped Wall Street’s estimates. Zooming out, we think this was a good quarter with some key areas of upside. The stock traded up 10.6% to $7 immediately following the results.

Orion had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is just one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .